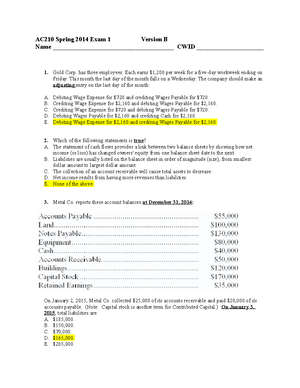

- Information

- AI Chat

Chapter 1 handout - unit 1 notes

Intro To Accounting (AC 210)

University of Alabama

Preview text

AC 210 - CHAPTER 1

BUSINESS DECISIONS AND FINANCIAL ACCOUNTING

LO 1-1 Describe various organizational forms and business decision makers.

A. Understand the Business 1. Organizational Forms: a. ____________ – business owned by 1 person; owner is personally liable for all business debts b. ____________ – business owned by 2 or more people; they’re personally liable for all business debts c. ___________ – A separate entity from both a legal and accounting perspective. public or private business whose owners are not liable for business debts d. __________ – Other organizational forms exist, such as a limited liability company (LLC), which combines characteristics of a partnership and a corporation.

B. Accounting for Business Decisions 1. Most companies exist to earn profits for their stockholders; profits are earned by selling goods or services to customers for more than they cost to produce. 2. Accounting—A system of analyzing, recording, and summarizing the results of a business’s operating, investing, and financing activities and then reporting them to decision makers. 3. Accounting is the “__________________.” 4. Accountants assist in reporting financial information for decision making and help its owners understand the financial effects of those business decisions. 5. The accounting system produces two kinds of reports a. _____________ Accounting = ___________ focus i. Who are the users? ii. What do they use? iii. 2 primary functions:

- ____________ business activities of a company

- ____________ those measurements to relevant decision-makers b. __________ Accounting = ____________ focus i. Who are the users? _____________ ii. What do they use? _______________________

LO 1-2 Describe the purpose, structure, and content of the four basic financial statements.

A. The Basic Accounting Equation: _________________________________ The Equation Must Always Balance!!

B. Separate entity assumption—The financial reports of a business are assumed to include the results of only that business’s activities.

C. _________ – economic resources owned or controlled by a company (expected to ↑ cash inflows or ↓ outflows) 1. Things the company OWNS 2. Cash, Inventory, Supplies, Accounts Receivable, Land, Equipment, Furniture

D. __________ – an obligation, financial, or service-based, between two parties that hasn’t been fulfilled or paid in full (creditors) 1. What the company OWES to creditors 2. amount owed or debt = “payable” 3. Accounts Payable, Notes Payable, Interest Payable and other liabilities

E. ______________ – owners’ claims to a company’s resources (stockholders/shareholders) for two reasons: 1. ____________ - amounts they contributed to the business in exchange for its stock (). 2. ____________ - profits the company has earned through its operations (___).

F. Profits are generated when the total amount earned from selling goods and services is greater than all the costs incurred to generate those sales. 1. Revenues – amounts __________ from selling products or services to customers 2. Expenses – All _____________ when doing business that are necessary to earn revenues. 3. Net Income (a.k profit) – Revenues - expenses (if expenses exceed revenues, the result is called a _________). a. Income increases Equity (RE), Loss decreases Equity (RE) 4. Dividends – distributions of ______________ to owners; reported as a reduction in Retained Earnings. a. Dividends are not an expense incurred

G. Financial Statements 1. Reports prepared at any time during year. 2. Most commonly monthly, quarterly, and annually using calendar year or fiscal year (a 12-month period ending on a day other than December 31). 3. Each financial statement has a heading (name of company, name of statement, and time period). 4. Each major caption has an underlined subtotal; “bottom line” amount has a double underline. 5. Unit of measure assumption—Financial results of business activities should be measured and reported using a single monetary unit. 6. Accounts—A standardized format that organizations use to accumulate and report the dollar effects of each financial statement item.

H. There are four basic financial statements 1. ____________________ – reports a company’s revenues less expenses over a period of time a. Revenues are on top, usually with largest, most relevant revenue listed first, then expenses are subtracted, again from largest to smallest, except that Income Tax Expense is the last expense listed. b. Net Income = total revenues - total expenses. c. Single-step income statement format groups revenues separately from expenses and reports a single measure of income.

_____________________ - Help financial statement users understand how the amounts were derived and what other information may affect their decisions.

Relationships among the Financial Statements—The four basic financial statements connect to one another. a. Net income, from the income statement, is a component in determining ending Retained Earnings on the statement of retained earnings. b. Ending Retained Earnings is then reported on the balance sheet. c. Cash on the balance sheet is equal to the ending Cash reported on the statement of cash flows.

LO 1-3 Explain how financial statements are used by decision makers.

1

2

3

A. Using Financial Statements 1. Creditors - Mainly interested in assessing two things: a. Is the company generating enough cash to make payments on its loans? SCF b. Does the company have assets to cover its liabilities? B/S

- Investors - Expect a return on their contribution to the company: a. What is the immediate return (through dividends) on my contributions? SRE b. What is the long-term return (through stock price increases resulting from the company’s profits)? I/S

LO 1-4 Describe factors that contribute to useful financial information. A. Useful Financial Information 1. Generally Accepted Accounting Principles (GAAP) - rules used in the US to calculate and report information in the financial statements. a. FASB – independent organization with primary responsibility for establishing U. GAAP i. A company’s managers have primary responsibility for following GAAP. ii. All public companies hire independent auditors to scrutinize their financial records.

Main goal: Provide useful financial information to external users for decision making.

Ethical Conduct a. Ethics - The standards of conduct for judging right from wrong, honest from dishonest, and fair from unfair. b. Sarbanes-Oxley Act (SOX) - provides regulation of auditors and the services they offer; increases the accountability of corporate ______________; addresses conflicts of interest for securities analysts; and provides _____________ for violators

STATEMENT OF CASH FLOWS

For each activity, identify as a cash inflow or (outflow) and its proper classification on the statement of cash flows.

Activity Inflow or (Outflow) Operating Investing Financing

a. Cash paid to employees and suppliers

b. Cash used to buy equipment and software

c. Cash dividends paid to stockholders

d. Cash received from customers

e. Cash received from selling equipment

f. Cash borrowed from the bank

g. Cash from issuing stock

h. Cash paid for interest

SCF Example 1: The net cash flow provided by operating activities is an inflow of $49,000, the net cash flow used in investing activities is $17,000, and the net cash flow used in financing activities is $25,000. If the beginning cash account balance is $9,000, what is the ending cash account balance?

SCF Example 2: Ruggs’ Riggs reports the following: Cash collected from customers 10, Cash dividends paid to stockholders 6, Cash proceeds from sale of land 27, Cash proceeds from bank loan 15, Cash payments toward bank loan 3, Cash paid to purchase equipment 9,

Ruggs’ Riggs would report net cash provided (used) by investing and financing activities of: Investing $ Financing $___________

Preparing an Income Statement, Statement of Retained Earnings, and Balance Sheet

The following information was reported in the December 31 financial statements of Saban Airways, Inc. Some information within the balance sheet was lost. Assume Saban Airways, Inc. started the year with $13,517 in Cash, $3,725 in Accounts Payable and $5,370 in Retained Earnings. The company was profitable this year earning $430. Shareholders received $20 in dividend payments from the company.

List the Financial Statement equations.

Fill in the missing information for the December 31st Balance Sheet.

SABAN AIRWAYS, INC. Balance Sheet At December 31 (Amounts in millions)

Assets

Cash $ 2, Accounts Receivable * Supplies 680 Equipment 14, Total Assets *

Liabilities Accounts Payable $4, Notes Payable * Total Liabilities 11, Stockholders’ Equity Common Stock 1, Retained Earnings * Total Stockholders’ Equity 7, Total Liabilities and Stockholders’ Equity $18,

OVERVIEW OF FINANCIAL STATEMENTS

Identify the purpose (i. what is measured/reported) and equation used to complete each of the financial statements.

Financial Statement Purpose Equation Income Statement

Statement of Retained Earnings

Balance Sheet

Statement of Cash Flows

RELATIONSHIPS AMONG FINANCIAL STATEMENTS

Answer the following questions.

How does the income statement tie to the statement of retained earnings?

How does the statement of retained earnings tie to the balance sheet?

How does the balance sheet tie to the statement of cash flows?

Chapter 1 handout - unit 1 notes

Course: Intro To Accounting (AC 210)

University: University of Alabama

- Discover more from: