- Information

- AI Chat

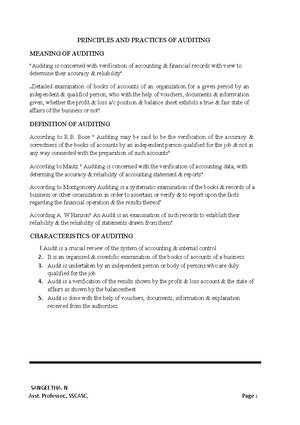

Accounting terminology

Auditing

Nalanda Open University

Preview text

Accounting terminology

The circumstances essential to the translation of fiscal reports are a figuring out (1) of the data expected by the specific client, (2) of the phrasing, and (3) of the guidelines or shows utilized by bookkeepers in their planning of budget summaries. The requirements of the different gatherings who use articulations have been proposed. Concerning wording, the two regions bewildering for the normal peruser however crucial for the comprehension of the asset report are the things that express the possession interest and the stores.

The possession interest of an ownership or association might be expressed in sums having a place with the one or a few proprietors or simply as the total assets. The aggregate sum is the abundance of the resources over the obligations of the worry. When added to the obligations, the aggregate equivalents the resources by definition. Custom puts the possession interest on the asset report headed liabilities or, all the more accurately, liabilities and proprietors' capital. The last option heading perceives the lawful distinction between the loan bosses, who have cases to fixed amounts of cash as of specific dates, and the proprietors, who are the leftover petitioners to resources and pay.

In a partnership's monetary record, the premium of the proprietor investors ought to be separated as between paid-in venture and resulting growths from profit left in the business. The previous show up as such a lot of capital stock, frequently at an erratic standard or expressed esteem, and any overabundance as abundance paid in by investors, paid-in excess, or

capital excess. The other piece of the possession value might show up as profit held in the business, benefit and misfortune, or procured excess. Acknowledgment that this sum is simply an equilibrium of significant worth and addresses the leftover case of the proprietors, which might be put resources into nonliquid resources, ought to forestall the typical confusion that excess is a pot of cash promptly accessible for profits or obligation installment.

Valuation holds

Rather than simply showing such a resource as plant and hardware at its net book esteem, it is standard to show its unique expense with an independently expressed measure of remittances for devaluation or, all the more confusingly, a hold for deterioration. Likewise, stipends for misfortunes on clients' obligations to the business might show as a derivation either for recompenses for terrible obligation misfortunes or a save for awful obligations. In the late twentieth century bookkeepers started utilizing the expression "stipend" as opposed to "hold" to clarify that these sums are appraisals of loss of significant worth and not money or assets.

Responsibility holds

Periodically a responsibility, particularly where the sum is unsure, shows up as a "hold." Subsequently, personal expense obligation might be called save for personal charges, albeit better practice is to mark the thing "assessed risk for" or "gathered" annual duties.

some precise reason for gauge exists, as on account of devaluation of machines and structures, awful obligation misfortunes, and the consumption of oil wells and mines. This cost rule is usually suspended when current resources have a market esteem underneath cost at the date of the monetary record. The ongoing resources are those resources that transform into cash over common activity in something like a year (longer in a couple of enterprises) and normally incorporate money, attractive protections, clients' obligation, and inventories. Attractive protections and inventories are regularly esteemed at whichever is lower, cost or market, halfway as an issue of traditionalism, which is itself very nearly a bookkeeping rule. This training is likewise a question of perceiving a worth misfortune that pays off current obligation paying influence. The estimation of this capacity is a focal object of explanation examination. Fixed resources, for example, plant or long haul security speculations not prone to be offered to meet obligation, are generally displayed at cost and overlook market esteem variances with the understanding that such vacillations are not critical to the "going concern." Examination and revaluation of the decent resources are not normal practice.

Numerous exceptional bookkeeping rules emerge from exchange customs, administrative guidelines, and duty regulations. They frequently apply just to the assertions of extraordinary sorts of organizations, like assembling, promoting, rail lines, public utilities, business banks, life, fire, and setback protection, and holding organizations. Since training fluctuates enormously, commonplace structures and wording are not steady in these different fields.

Accounting terminology

Course: Auditing

University: Nalanda Open University

- More from:AuditingNalanda Open University18 Documents