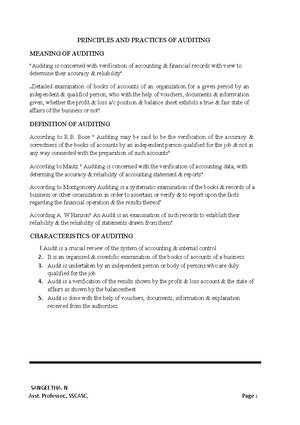

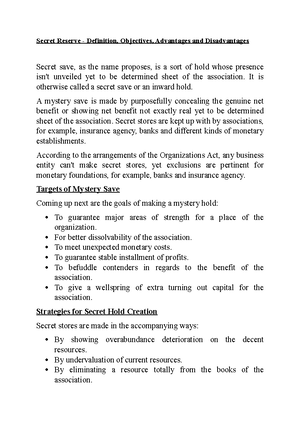

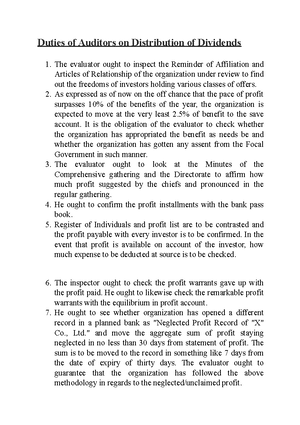

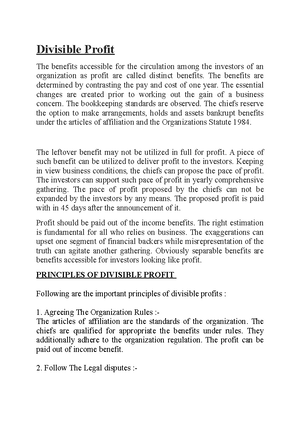

- Information

- AI Chat

Accounting

Auditing

Nalanda Open University

Preview text

Accounting

Bookkeeping, orderly turn of events and investigation of data about the monetary undertakings of an association. This data might be utilized in various ways: by an association's chiefs to help them plan and control progressing tasks; by proprietors and official or administrative bodies to assist them with evaluating the association's exhibition and pursue choices regarding its future; by proprietors, loan specialists, providers, workers, and others to assist them with concluding how long or cash to dedicate to the organization; by legislative bodies to figure out what burdens a business should pay; and sometimes by clients to decide the cost to be paid when agreements call for cost-based installments.

Bookkeeping gives data to this large number of motivations through the support of information, the investigation and understanding of these information, and the arrangement of different sorts of reports. Most bookkeeping data is verifiable — that is, the bookkeeper sees movements of every kind that the association embraces, records their belongings, and gets ready reports summing up what has been recorded; the rest comprises of gauges and plans for current and future periods.

Bookkeeping data can be created for any sort of association, not only for exclusive, benefit looking for organizations. One part of bookkeeping manages the financial tasks of whole nations. The rest of this article, in any case, will be given fundamentally to business bookkeeping.

The goals and qualities of monetary announcing

The general target of monetary announcing, which incorporates the creation and scattering of monetary data about the organization as fiscal reports, is to give helpful data to financial backers, lenders, and other closely involved individuals. In a perfect world, bookkeeping data gives organization investors and different partners (e., representatives, networks, clients, and providers) with data that guides in the expectation of the sums, timing, and vulnerability of future incomes. Also, fiscal reports reveal insights about monetary assets and the cases to those assets.

As of late, there has been a developing interest with respect to

partners for data concerning the social effects of corporate

independent direction. Progressively, organizations are including extra

data about natural effects and dangers, representatives, local area

association, humanitarian exercises, and customer security. A

significant part of the detailing of such data is willful, particularly in the US.

What's more, quantitative information are currently enhanced with

exact verbal portrayals of business objectives and exercises. In the

US, for instance, public corporations are expected to outfit a record

ordinarily recognized as "the board's conversation and examination"

as a feature of the yearly report to investors. This record sums up verifiable execution and incorporates forward-looking data.

To bookkeepers, the two most significant qualities of valuable data

are importance and dependability. Data is pertinent to the degree that

it might possibly change a choice. Pertinent data further develops

forecasts of future occasions, affirms the result of a past expectation,

and ought to be accessible before a choice is made. Dependable data

is undeniable, authentically unwavering, and impartial. The sign of nonpartisanship is request bookkeeping data not be chosen to help one

class of clients to the disregard of others. While bookkeepers perceive

a tradeoff among significance and unwavering quality, data that needs

both of these attributes is viewed as deficient for direction.

Accounting

Course: Auditing

University: Nalanda Open University

- More from:AuditingNalanda Open University18 Documents