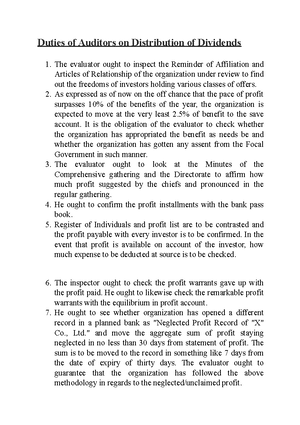

- Information

- AI Chat

Capital and interest

Auditing

Nalanda Open University

Preview text

Capital and interest

Capital and premium, in financial matters, a supply of assets that might be utilized in the development of labor and products and the

cost paid for the utilization of credit or cash, separately.

Capital in financial matters is an expression of numerous

implications. They all suggest that capital is a "stock" by diverge from

pay, which is a "stream." In its broadest conceivable sense, capital

incorporates the human populace; nonmaterial components like abilities, capacities, and training; land, structures, machines, hardware

of numerous sorts; and all supplies of merchandise — got done or

incomplete — in the possession of the two firms and families.

In the business world the word capital as a rule alludes to a thing yet

to be determined sheet addressing that piece of the total assets of an undertaking that has not been delivered through the tasks of the

endeavor. In financial aspects the word capital is by and large bound

to "genuine" rather than simply "monetary" resources. Different as the

two ideas might appear, they are not inconsequential. On the off

chance that all monetary records were merged in a shut financial

framework, all obligations would be counteracted in light of the fact

that each obligation is a resource in one asset report and a responsibility in another. What is left in the united monetary record, in

this way, is a worth of the relative multitude of genuine resources of a

general public on one side and its all out total assets on the other. This

is the financial specialist's idea of capital.

A differentiation might be made between products in the possession of

firms and merchandise in the possession of families, and endeavors

have been made to limit the term capital construction to the previous. There is likewise a differentiation between products that have been

delivered and merchandise that are gifts of nature; endeavors have

been made to bind the term funding to the previous, however the

qualification is difficult to keep up with practically speaking. Another significant differentiation is between the supply of people (and their

capacities) and the load of nonhuman components. In a slave society

people are included as capital similarly as domesticated animals or

machines. In a free society each man is his own slave — the worth of

his body and brain isn't, consequently, an article of business and

doesn't get into the bookkeeping framework. In severe rationale

people ought to keep on being viewed as a feature of the capital of a general public; however by and by the qualification between the piece

of the all out stock that goes into the bookkeeping framework, and the

part that doesn't, is critical to such an extent that it isn't is really to be

expected that numerous journalists have prohibited people from the

capital stock.

Another differentiation that has some verifiable significance is that among coursing and fixed capital. Fixed capital is typically

characterized as that which doesn't alter its structure in that frame of

mind of the course of creation, like land, structures, and machines.

Coursing capital comprises of products in process, unrefined

components, and loads of completed merchandise ready to be sold;

these merchandise should either be changed, as when wheat is ground into flour, or they should change possession, as when a supply of

products is sold. This differentiation, in the same way as other others,

is generally difficult to keep up with. In any case, it addresses an

unpleasant way to deal with a significant issue of the overall design of

capital; that is, of the extents where products of different sorts are

found. The supply of genuine capital displays solid

complementarities. A machine is of no utilization without a gifted administrator and without unrefined components for it to deal with.

The traditional hypothesis of capital

particularly made a sharp qualification between capital as "delivered

method for creation," and land as the "first and indestructible powers

of the dirt." In current financial matters this differentiation has become obscured.

Interest

By and large, the idea of capital has been so firmly bound to the idea of interest that it appears to be astute to take these two subjects together, despite the fact that in the cutting edge view it is capital and pay as opposed to capital and interest that are the connected ideas.

Interest as a type of pay might be characterized as pay that is gotten because of the ownership of legally binding commitments for installment with respect to another. Interest, all in all, is pay that is gotten because of the responsibility for bond, a promissory note, or some other instrument that addresses a commitment with respect to another party to pay aggregates from here on out. The commitments might take many structures. On account of the interminability, the endeavor is to pay a specific aggregate every year or other timespan for the endless future. A bond with a date of development as a rule includes a guarantee to pay a specific total every year for a given number of years, and afterward a bigger aggregate on the deadline. A promissory note habitually comprises of a guarantee to pay a solitary total at a date that is sooner or later.

In the event that a1, a2,... an are the aggregates gotten by the bondholder in years 1, 2... n, and assuming P0 is the current worth in year 0, or the total for which the security is bought, the pace of interest r in the entire exchange is given by the situation.

There is no broad answer for this situation, however by and by it very well may be tackled effectively by progressive estimate, and in

extraordinary cases the condition decreases to a lot easier structures. On account of a promissory note, for example, the condition decreases to the structure,

Where an is the single guaranteed installment. On account of an unendingness with a yearly installment of a, the recipe lessens to.

In this manner in the event that one needed to pay $200 to buy a ceaseless annuity of $5 per annum, the pace of revenue would be 2 1/2 percent.

It ought to be seen that the components of the pace of revenue are those of a pace of development. The pace of revenue isn't a cost or proportion of trade; it not set in stone on the lookout. Still up in the air in the market is the cost of legally binding commitments or "securities." The higher the cost of a given legally binding commitment, the lower the pace of revenue on it. Assume, for example, that one has a promissory note that is a guarantee to pay one $100 in one year's time. In the event that I purchase this for $100 now, the pace of revenue is zero; assuming I get it for $95 now the pace of revenue is a little more than 5%; on the off chance that I get it for $ now, the pace of revenue is around 11%. The pace of revenue might be characterized as the gross pace of development of capital in a legally binding commitment.

A qualification is generally made among interest and benefit as types of pay. In common discourse, benefit normally alludes to pay got

In the structure of old style financial aspects, crafted by Nassau Senior merits notice. He brought up the issue whether benefit or interest "paid for" anything; that is, whether there was any recognizable commitment to the overall result of society that wouldn't be impending in the event that this type of pay were not paid. He distinguished such a capability and called it restraint. Karl Marx denied the presence of any such capability and contended that the social item should be credited completely to demonstrations of work, capital being simply the epitomized work of the past. On this view, benefit and interest are the consequence of unadulterated double- dealing as in they comprise of a pay got from the power position of the entrepreneur and not from the exhibition of any help. Non- communist business analysts have commonly followed Senior in discovering some capability in the public eye that relates to these types of pay.

The Marginalists for the most part held that benefit and interest were connected with the minimal efficiency of the expansion of the time of creation. Böhm-Bawerk expected to be that "indirect" cycles of creation would commonly be more useful than processes with more limited times of creation; he thought there was an efficiency of "standing by" (to utilize the term of Alfred Marshall) and considered the pace important to be an incitement to the entrepreneur to expand the time of creation.

A low pace of revenue prompts focus on longer, more indirect cycles, and a high pace of interest on more limited, less indirect cycles. There is a cutoff, in any case, on the time of creation forced by the current supply of gathered capital. On the off chance that one sets out on a long cycle with inadequate capital, he will find that he has depleted his assets before the finish of the interaction and before the natural products can be assembled. It is the matter of the pace important to forestall this, and to change the indirectness of the cycles used to the capital assets accessible. The Marginalists' hypothesis of interest arrived at its most clear articulation in crafted by Irving Fisher. He saw a balance pace of still up in the air by the collaboration of two

arrangements of powers: the eagerness of customers from one perspective, and the profits from expanding the time of creation on the other.

John Maynard Keynes brought another methodology. His liquidity inclination hypothesis of premium is a short-run hypothesis of the cost of legally binding commitments ("securities"), and it is basically a utilization of the overall hypothesis of market cost. If individuals all in all conclude that they need to hold a bigger extent of their resources as cash, and on the off chance that new cash isn't made to fulfill this longing, there will be a net craving to sell protections and the cost of protections will fall. This is exactly the same thing as an ascent in the pace of interest. Alternately, to dispose of cash the cost of protections will increase and the pace of revenue will fall. This, then, at that point, is the hypothesis of the "market" pace of revenue, by stand out from the Marginalists' hypothesis, which worries about whether there is a long-run harmony pace of revenue. The contention, subsequently, between the liquidity inclination hypothesis — which sees revenue as a "pay off" to forestall individuals holding cash as opposed to bonds — and the time inclination hypothesis — which views revenue as a pay off to convince individuals to defer delights to the future — can be settled by putting the previous in the short run and the last option over the long haul.

Contemporary inquiries

The center of the twentieth century saw a significant change in the focal point of concern connecting with the hypothesis of interest. Financial specialists appeared to lose revenue in the balance hypothesis, and their primary concern was with the impact of paces of interest as a piece of money related strategy in the control of expansion. It was perceived that the money related authority had some control over the pace of revenue in the short run. The debate lay predominantly between the supporters of "money related strategy" and the promoters of "financial approach." Assuming that expansion is viewed as a side effect of a longing with respect to a general public to consume and put more altogether than its assets grant, obviously the issue can be gone after either by reducing venture or by lessening

may, is the situation for specialization. There is an interest for the overwhelming majority various levels of possession and obligation, and premium bearing commitments tap a market that would be difficult to reach with value protections; they are likewise unconventionally very much adjusted to the commitments of states. The essential legitimization for endlessly interest bearing protections is that they give a simple and advantageous way for gifted executives to control capital that they don't possess and for the proprietors of money to surrender its control. The cost society pays for this plan is interest.

There stays the issue of the socially ideal pace of interest. It very well may be contended that it is a waste of time to follow through on any greater expense than one requirements to and that the pace of revenue ought to be basically as low as is steady with the exhibition of the capability of the monetary business sectors. This position, obviously, would put all the weight of control of monetary changes on the financial framework, and it is sketchy whether this would be OK strategically.

The antiquated issue of "usury," as the abuse of the uninformed poor by moneylenders, is as yet significant in many regions of the planet. The cure is the improvement of satisfactory monetary establishments for the necessities of all classes of individuals as opposed to the endeavor to preclude or even to restrict the taking of interest. The perplexing design of loaning foundations in a created society — banks, building social orders, land banks, helpful banks, credit associations, etc — vouches for the truth of the help that the moneylender gives and that premium pays to. The democratization of credit — that is, the augmentation of the force of getting to all classes in the public eye — was one of the significant social developments of the twentieth 100 years.

Capital and interest

Course: Auditing

University: Nalanda Open University

- Discover more from:AuditingNalanda Open University18 Documents

- More from:AuditingNalanda Open University18 Documents