- Information

- AI Chat

Audit Risk issue - Student version

Association of Chartered Certified Accountants - ACCA (PAC150)

INTEC Education College

Recommended for you

Preview text

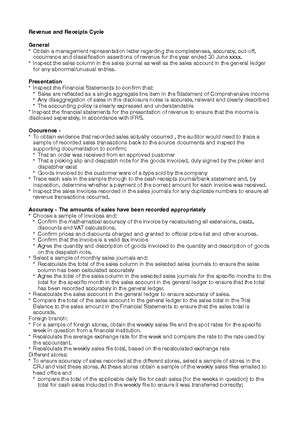

AUDIT RISK

Issue in Q Audit Risk Audit Response 1 Co. may not include inventory quantity from all warehouse into their records. - 10 warehouse

If the co. did not include all inventories in 10 warehouse in their records, then INVENTORY might be understated.

Obtain list of all inventory in 10 warehouse and make sure it is included in final inventory listing.

2 Co. introduced perpetual inventory count where all inventory must be counted at least once during the year.

If the co. did not count their inventory once a year, then inventory might be MATERIALLY MISSTATED.

Obtain Inventory count sheet for the inventory count performed during the year.

Ensure physical same as in the system. / no discrepancies. 3 Co. have a lot of old trade debtors, which pay slowly.

If the co. did not provide sufficient allowance for DD, Then trade receivable might be overstated.

Inspect POST YEAR END PAYMENT RECEIVED from old debtor if any to assess whether old balance is recovered.

Inspect trade rec. ageing to identify amount of long outstanding debt. 4 Co. released entire bad debt provision.

If the co. released BD provision while it is not VIRTUALLY CERTAIN, then TRADE RECEIVABLE is overstated.

Obtain bank statement for any payment received. And obtain correspondence from the debtor. 5 Co. issues shares at premium.

If the co. did not split between SC and SP, then SC will be overstated.

Recalculate SC and SP amount and agree to the FS to verify accuracy.

6 Co. took long term loan from the bank.

If the. Co did not split loan amount between CL and NCL,

Then NCL or CL might be overstated.

Recalculate the split between CL and NCL based on the loan agreement and agree to FS.

Co. in negotiation process to obtain loan.

The co. might manipulate their FS to be able to get the loan hence FS as a whole could contain MM.

Apply professional scepticism while auditing the FS.

Perform extensive Substantive procedure. 7 The loan carried interest rate of 5% per annum.

If the co. wrongly calculate its interest, then interest expense might be materially misstated.

Recalculate interest expenses based on loan agreement and agree to the figure in FS.

8 Employee took legal case on company. If there is probable chance to lose the case.

If the co. did not recognise provision for legal action,

Then PROVISION might be understated

Enquire co’s lawyer on the probability of the legal case and if it is probable, ensure sufficient provision recognise.

9 Employee took legal case on company. If there is possible chance to lose the case.

If the co. did not disclose contingent liability for legal action,

Then FS contain material misstatement.

Enquire co’s lawyer on the probability of the legal case and if it is possible, ensure sufficient disclosure.

Employee took legal case on company.

If the co. did not recognise provision for legal action WHEN IT IS PROBABLE ,

Then PROVISION might be understated. 10 Co. close one of it factory (division/ branch) and made employees redundant.

If the co. did not recog. sufficient redundancy provision for employees, then provision is understated.

Obtain list of all employees made redundant and recalculate provision for redundancy. Agree the calculation to FS.

11 Co. obtain IREDEEMABLE PREFERENCE SHARE.

If the co. recognise this as liability instead of equity, then Liability will be overstated.

Obtain the share agreement for the irredeemable pref. share and agree to FS on its classification in equity.

Co. obtain convertible bond.

If the co. did not split between ___ and _____, then E or L might be overstated.

Obtain the agreement for the convertible bond and perform the recalculation of the split.

Compare to amt in FS for any difference. 12 Co. paid huge director remuneration to directors and it has to be disclosed in FS per IAS.

If the co. did not disclosed as per IAS, then FS might be MM.

Inspect FS on the directors remuneration disclosure to assess if it is as per IAS.

13 Financial controller / Director left the company during the year and his role shared among finance team.

If FC left the co then no one will review the FS. Therefore, FS as a whole could contain MM.

Apply prof scepticism when auditing FS and perform extensive SP on risky area.

14 No supplier statement reconciliations/ bank recon/ receivable recon... done.

DETECT AND CORRECT ERROR

If the co. did not perform SUPPLIER reconciliation then any error will not be detected and corrected.

Then, TRADE PAYABLE could be materially misstated.

If the co. did not perform debtor reconciliation then any error will not be detected and corrected.

Then, TRADE REC could be materially misstated.

If the co. did not perform BANK reconciliation then any error will not be detected and corrected.

Then, BANK BALANCE could be materially misstated.

Ask the co. to perform the ____ reconciliation and ensure any error detected is corrected in FS.

25 Co. made revaluation of property and gain recognised under other income.

Gain in revaluation = OTHER COMPREHENSIVE INCOME

If the co. recognise gain on revaluation under other income instead of OCI, then other income will be overstated.

Ask them to reclass this gain on revaluation to OCI.

Recalculate the gain to ensure accuracy.

26 Co. ordered large no. of non-current assets but not received yet.

If the co. record PPE which is still not yet received, then PPE will be overstated.

Physically inspect the NEW ASSET recognised to ensure existence.

27 Co. holds a lot of old PPE.

RA < CA

If the co. didn’t review the old asset for impairment, then PPE will be overstated.

Inspect impairment review document done by management to assess if write down is necessary.

28 Co had an old asset which was refurbished recently.

If the co. capitalised revenue expenditure during refurbishment, then PPE will be overstated.

Obtain breakdown of refurbishment and inspect the nature of the expenses. Ensure all REV. EX. Expensed off.

29 Co had disposed NCA recently.

If the co. didn’t remove the disposed asset from NCA Register, then PPE will be overstated.

Inspect NCA Register to ensure all disposed asset has been removed.

30 Co had disposed NCA recently. - Gain or loss on disposal.

If the co. wrongly calculate gain or loss on disposal, then profit will be misstated.

Recalculate the gain or loss on disposal to ensure accuracy.

31 Co had done revaluation of property at year end.

= revalue ALL class of asset.

If the co. did not revalue the asset within the same class, then PPE might be MM.

Inspect NCA Register to verify if all asset within the same class already being revalued.

32 Co.’s PPE was damaged in flood or natural disaster.

If the co. didn’t review the damaged asset for impairment, then PPE will be overstated.

Inspect impairment review document done by management to assess if write down is necessary.

33 Co has too many old inventory.

If the co. didn’t review the old inventory for impairment, then Inventory will be overstated.

Inspect impairment review document done by management to assess if write down is necessary.

34 Co incurred development

If the co. capitalised cost that did not meet CAPITALISATION

Obtain breakdown of development cost incurred to assess its

expenditure, to develop new product.

Ias 38 : intangible asset.

CRITERIA (pirate) as per IAS 38, then IA will be overstated.

NATURE of the cost. Only cost that meet CC should be capitalised.

35 Co. incurred research expenditure which was capitalised.

Ias 38 : intangible asset.

RESEARCH = DR EXP CR CASH

DEVELOPMENT = DR IA CR CASH

The company should not capitalised research cost ; which will overstate its intangible asset.

Ask them to removed the research cost from IA and recognise as expenses.

36 Co. sold inventories at huge discounts during the year.

If the co. did not value its inventory to the lower of cost or NRV, then inventory might be overstated.

Compare cost of inventory against its selling price to assess if write down is necessary.

37 Co use standard cost to value inventory.

If the standard costing for inventory is not being reviewed regularly, inventory balance may be materially misstated.

Obtain latest standard costing valuation and discuss with management how frequent the std costing being reviewed and updated. 38 WIP valued using percentage of completion.

If the management overestimate the stage of completion, then inventory is overstated.

Obtain the calculation or report on stage of completion and recalculate the WIP balances based on percentage of completion to confirm accuracy. 39 Co introduce new inventory system during the year.

If the transferred figures to the new system is incorrect , the inventory maybe materially misstated.

Enquire management and ascertain how they monitored that inventory transfer process from old to new system

40 Co has many warehouses in which inventory counts is done.

Co may not be able to confirm count is done properly in all location. The inventory maybe materially misstated in terms of quantity or value.

Obtain stock count sheets from all warehouses and inspect the inventory listing to see it has been updated

41

When too many indication that the company may facing going concern issue - can relate to poor ratio

This shows that the co. facing GC issue.

If the company did not disclose their material uncertainty adequately is FS, then FS contain MM.

Perform going concern review on the company by obtaining their forecasted cash flow forecast for the next 5 years.

If there is material uncertainty, ensure adequately disclosed in FS.

Audit Risk issue - Student version

Course: Association of Chartered Certified Accountants - ACCA (PAC150)

University: INTEC Education College