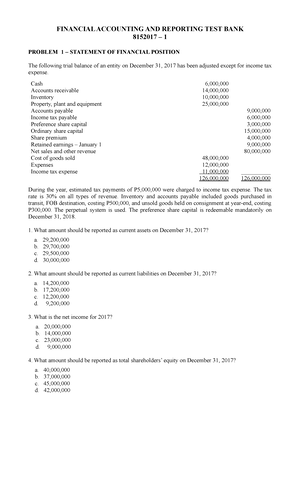

- Information

- AI Chat

IAS 40 Investment property F7

Association of Chartered Certified Accountants - ACCA (PAC150)

INTEC Education College

Recommended for you

Related Studylists

IAPreview text

INVESTMENT PROPERTY (IAS 40)

DEFINITIONS OF KEY TERMS

Investment property.

Land or building, or part of a building, or both, held by the owner or the lessee under a finance lease to earn rentals and/or for capital appreciation, rather than for use in production or supply of goods and services or for administrative purposes or for sale in the ordinary course of business.

Owner-occupied property.

Property held by the owner or the lessee under a finance lease for use in production or supply of goods and services or for administrative purposes.

Note: One of the distinguishing characteristics of investment property (compared to owner- occupied property) is that it generates cash flows that are largely independent from other assets held by an entity. Owner-occupied property is accounted for under IAS 16, Property, Plant, and Equipment.

Note: An asset held by an entity as a right-of -use asset under IFRS 16 and leased out under an operating lease is treated as investment property.

Example XYZ Inc. and its subsidiaries have provided you, their International Financial Reporting Standards (IFRS) specialist, with a list of the properties they own:

Land held by XYZ Inc. for undetermined future use

A vacant building owned by XYZ Inc. and to be leased out under an operating lease

Property held by a subsidiary of XYZ Inc., a real estate firm, in the ordinary course of its business

Property held by a subsidiary of XYZ Inc., a real estate firm, in the ordinary course of its business

Property held by XYZ Inc. for the use in production

A hotel owned by ABC Inc., a subsidiary of XYZ Inc., and for which ABC Inc. provides security services for its guests’ belongings

Required

Advise XYZ Inc. and its subsidiaries as to which of the aforementioned properties would qualify under IAS 40 as investment properties. If they do not qualify thus, how should they be treated under IFRS?

Solution

Pr operties described under items 1, 2, and 5 would qualify as investment properties under IAS 40. With respect to item 5, it is to be noted that IAS 40 re quires that when the ancillary services are provided by the entity and they are considered a relatively insignificant component of the arrangement, then the property is considered an investment property.

These properties qualify as investment properties because they are being held for rental or for capital appreciation as opposed to actively managed properties that are used in the production of goods.

Property described in item 3 is to be treated as “inventory” under IAS 2.

Property described in item 4 is treated as a long-lived asset under IAS 16.

RECOGNITION

Investment property shall be recognized as an asset when and only when

- It is probable that future economic benefits will flow to the entity.

- The cost of the investment p roperty can be measured reliably.

Recognition principles are similar to those contained in IAS 16.

MEASUREMENT

Measurement at Recognition

An investment property shall be measured initially at cost, including transaction charges. Again, the principles for determining cost are similar to those contained in IAS 16, in particular for replacement and subsequent expenditure.

If an entity measures investment property at fair value, it shall continue to do so until disposal, even if readily available market data become less frequent or less readily available.

Cost Model An entity that selects the cost model shall measure all of its investment property in accordance with IAS 16’s requirements for that model except those classified as held-for-sale in accordance with IFRS 5.

Example Investors Galore Inc., a listed company in Germany, ventured into the construction of a mega shopping mall in south Asia, which is rated as the largest shopping mall of Asia. The company’s board of directors after market research decided that instead of selling the shopping mall to a local investor, who had approached them several times during the construction period with excellent offers, which he progressively increased during the year of construction, the company would hold this property for the purposes of earning rentals by renting out space in the shopping mall to tenants. For this purpose it used the services of a real estate company to find an anchor tenant (a major international retail chain) that then attracted other important retailers locally to rent space in the mega shopping mall, and within months of the completion of the construction the shopping mall was fully rented out.

The construction of the shopping mall was completed and the property was placed in service at the end of 20X1. According to the company’s engineering department the computed total cost of the construction of the shopping mall was $100 million. An independent valuation expert was used by the company to fair value the shopping mall on an annual basis. According to the fair valuation expert the fair values of the shopping mall at the end of 20X1 and at each subsequent year-end thereafter were

20X1 $100 million

20X2 $120 million

20X3 $125 million

20X4 $115 million

The independent valuation expert was of the opinion that the useful life of the shopping mall was ten years and its residual value was $10 million.

Required

What would be the impact on the profit and loss account of the company if it decides to treat the shopping mall as an investment property under IAS 40

a. Using the fair value model.

b. Using the cost model.

(Since the rental income for the shopping mall would be the same under both the options, for the purposes of this exercise do not take into consideration the impact of the rental income from the shopping mall on the net profit or loss for the period.)

Solution

(a) Fair value model

If the company chooses to measure the investment property under the fair value model it will have to recognize in net profit or loss for each period changes in fair value from year to year. Thus the impact on profit or loss for the various years would be

Year Cost Fair value Profit and loss 2001 100 100 0 2002 120 20 2003 125 5 2004 115 (10) (b) Cost model

If the company decided to measure the investment property under the cost model it would have to account for it under IAS 16 using the cost model prescribed under that Standard (which requires that the asset should be carried at its cost less accumulated depreciation and any accumulated impairment losses). Therefore, when investment property is measured under the cost model, the fluctuations in the fair value of the investment property from year to year would have no effect on profit or loss of the entity. Instead, the annual depreciation, which is computed based on the acquisition cost of the investment property will be the only charge to net profit or loss for each period (unless there is impairment which will also be a charge to net profit or loss for the year).

Based on the acquisition cost of $100 million (assuming there is no subsequent expenditure that would be capitalized), a residual value of $10 million, a useful life of ten years, and using the

The statement of profit or loss will include depreciation of $6,000.

(b) Fair value model

The property will be included in the statement of financial position at its fair value of $1,300,000.

The statement of profit or loss will include a profit of $290,000 ($1,300,000 – $1,010,000) in respect of the fair value adjustment. (Remember: this treatment of revaluation of an investment property differs from the accounting treatment of a revaluation gain for other non-current assets under IAS 16).

Example Suppose that the investment property in the previous example was sold in Year 2 for $1,550,000, and that selling costs were $50,000.

Required

What amounts would be included in the statement of profit or loss for Year 2 in respect of this disposal under

(a) the cost model and

(b) the fair value model?

Answer

(a) Cost model $

Sale value 1,550,

Selling costs (50,000)

––––––––––

Net disposal proceeds 1,500,

Minus: Carrying amount (1,004,000)

––––––––––

Gain on disposal 496,

––––––––––

(b) Fair value model $

Sale value 1,550,

Selling costs (50,000)

––––––––––

Net disposal proceeds 1,500,

Minus: Carrying amount (1,300,000)

––––––––––

Gain on disposal 200,

–––––––––

Transfers

Transfers to and from investment property shall be made when and only when there is a change of use evidenced by

- Commen cement of owner occupation (transfer from investment property to property, plant, and equipment)

- Commencement of development with a view to sale (transfer from investment property to inventories)

- End of owner occupation (transfer from property, plant, and equipment to investment property)

- Commencement of an operating lease to another party (transfer from inventories or property, plant, and equipment to investment property)

In cases where the fair value model is not used, transfers between classifications are made at the carrying value: the lower of cost and net realizable value if inventories, or cost less accumulated depreciation and impairment losses if property, plant, and equipment.

If owner-occupied property is transferred to investment property that is to be carried at fair value, then, up to the change, IAS 16 is applied. That is to say, any revaluation in fair value is treated in accordance with IAS 16.

However the building will be subjected to a fair value exercise at each year end and these gains or losses will go to profit or loss. If at the end of the following year the fair value of the building is found to be $380,000, $30,000 will be credited to profit or loss.

Disposals

Derecognise (eliminate from the statement of financial position) an investment property on disposal or when it is permanently withdrawn from use and no future economic benefits are expected from its disposal.

Any gain or loss on disposal is the difference between the net disposal proceeds and the carrying amount of the asset. It should generally be recognised as income or expense in profit or loss.

Compensation from third parties for investment property that was impaired, lost or given up shall be recognised in profit or loss when the compensation becomes receivable.

Disclosure requirements

These relate to:

Choice of fair value model or cost model Criteria for classification as investment property Assumptions in determining fair value Use of independent professional valuer (encouraged but not required) Rental income and expenses Any restrictions or obligations (IAS 40: paras. 74–79) Fair value model – additional disclosures

An entity that adopts this must also disclose a reconciliation of the carrying amount of the investment property at the beginning and end of the period. (IAS 40: paras. 77–78)

Cost model – additional disclosures

These relate mainly to the depreciation method. In addition, an entity which adopts the cost model must disclose the fair value of the investment property

Chapter end exercise

Q1 What is the definition of an investment property according to IAS 40 Investment Property?

A An investment in land and or buildings whether let to third parties or occupied by an entity within a group

B A property owned and occupied by an entity for its own purposes

C A property which is held to earn rentals or for capital appreciation

D An investment in land and or buildings other than leased property

Q2 IAS 40 Investment Property gives examples of investment properties, which include some of the following:

(1) Property held for long-term capital appreciation

(2 ) Property leased to another entity on a finance lease

(3) Property leased out under one or more operating leases

(4) Owner-occupied property

(5) Land held for an undetermined future use

(6) Property occupied by employees

Which of the above are listed by IAS 40 as examples of an investment property?

A 1, 5 and 6

B 1, 3 and 5

C 2, 3 and 4

D 2, 4 and 6

Q6 Identify, by clicking on the relevant box in the table whether each statement regarding IAS 40 Investment Property is true or false.

Investment property is held for administrative purposes TRUE FALSE

Investment property is property held for use in the supply of services TRUE FALSE

Investment property is property held for use in the production of goods TRUE FALSE

Investment property is property held by owner to earn rental income or for capital appreciation

TRUE FALSE

IAS 40 Investment property F7

Course: Association of Chartered Certified Accountants - ACCA (PAC150)

University: INTEC Education College

- Discover more from: