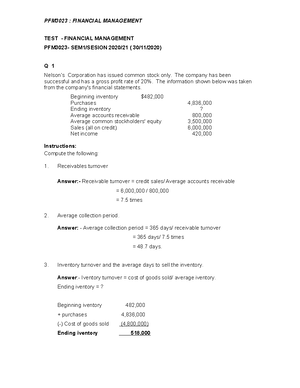

- Information

- AI Chat

Accounting equation - tutorial

Account (AA101)

Kolej Poly-Tech MARA BANGI

Recommended for you

Preview text

LECTURE

THE ACCOUNTING EQUATION

What the business owns – what the business owes = What the business is worth.

This is the key to understanding many of the aspects of accounting

To start trading, a business needs resources.

Assume that the owner supplies all the resources. (Internal sources)

Resources supplied by the owner = Resources in the business Therefore: the equation is: Capital = Assets

BUT: Usually, people other than the owner have supplied some of the assets, e. banks, suppliers. (External sources)

Amounts owing to these people = Liabilities

So, the equation changes to:

Assets = Capital + liabilities

Both sides will always equal each other

Assets

They are resources an entity controls as a result of past events and from which future economic benefits are expected to flow.

(a) Current assets – assets which are expected to be realised in the business normal course of trading e. inventory, debtors - accounts receivables, cash.

(b) Non-current assets – any tangible or intangible asset acquired on a long term basis to be used in providing a service to the business e. land & buildings, motor car, plant & machinery.

Liabilities

A liability is an entity’s present obligation arising from a past event, the settlement of which will result in an outflow of economic benefits from the entity.

(a) Current liabilities – liabilities which are payable within 12 months of the reporting date e. creditors - accounts payables, bank overdraft, short term loans.

(b) Non-Current liabilities – liabilities payable more than 12 months after the reporting date e. long term loan.

Capital

There are three meanings to Capital:

Capital represents the amount of money invested by the owner(s) in the business.

Capital represents the amount of money owed by the business to the owner.

From an accounting viewpoint, the business is always treated as a separate entity to the owner (Entity concept).

The important point to note is that we must think of capital as being a liability, although a rather special liability.

Capital is an Internal Liability, whereas money owed to an outsider can be classified as an External Liability.

- Capital shows how much the business is worth and is often described as the Net Worth of the business.

It will increase each year by any new capital injected into the business and by the profit made by the business and will decrease by any loss.

It will decrease by any amounts withdrawn from the business by the owner.

Example 1

Day One: Peter set up a fruit business by investing €500 of his money and borrowing €1,000 from the bank. He uses this €1,500 to buy stock of fruit which he intends to sell.

The Accounting Equation on day one is:

Assets Capital Liabilities

Inventory €1,500 = €500 + Bank Loan €1,

Day Two: Peter sells half of the inventory for €1,250 cash making a profit of €500. The Accounting equation on Day two is;

Assets Capital Liabilities

Inventory € Cash €1, €2,000 = €1,000 + €1,

Notice how the profit of €500 has increased the value of the business, i. the capital has risen from €500 to €1,000.

Day Three: The fruit has begun to perish and Peter is forced to sell off the remainder of the fruit for €550 cash. This is a loss of €200.

Assets Capital Liabilities

Cash €1,800 = €800 + €1,

Notice how the loss of €200 has reduced the value of the business, i. the capital has fallen to €800.

Assets and Liabilities are classified in the Statement to aid the owners, creditors, managers and other interested parties in understanding the financial position of the business.

Example 2

Pat Fox starts a business on the 1 January 2015 by investing €10,000 of his money in a business bank account.

On January 2 Pat receives a €50,000 mortgage from the bank which he uses to buy buildings.

On the 3 January 2015 Pat buys goods for resale for €6,000. He pays for the goods by cheque.

On the 4 January Pat sells half the inventory for €3,000 on credit to George Smith.

On the 5 January 2015 Pat buys €10,000 worth of goods for resale on credit.

On the 6 January 2015, a customer pays Pat €2,000 by cheque

On the 8 January 2015 Pat sells €5,000 worth of goods for €8,000 and is paid by cheque.

By now it should be clear that every transaction affects at least two items in the Statement of Financial Position, yet the SFP always balances because of the accounting equation.

Example 3

1 May 2015, B. Blake started a business and deposited €60,000 in a bank account opened for the business.

3 May 2015, Blake buys a shop for €32,000 paying by cheque.

6 May 2015, Blake buys some goods for €7,000 from D and he agrees to pay for them some time within the next two weeks.

10 May 2015, goods which cost €600 were sold to J. Browne for the same amount, the money to be paid later.

13 May 2015, goods which cost €400 were sold to D. Daley for the same amount. Daley paid for them immediately by cheque.

15 May 2015, Blake pays a cheque for €3,000 to D Smith in part payment of the amount owing.

31 May 2015, J. Browne who owed Blake €600, makes a part payment of €200 by cheque.

Detailed presentation of Blake’s Statement of Financial Position at 31 May 2015.

Blake - Sole Trader: Statement of Financial Position as at 31 May 2015 Assets € € Non-current assets Buildings 32, Current assets Inventory 6, Accounts Receivables 400 Cash at bank 25, 32,

Assets 64,

Capital and Liabilities Capital 60, Current liabilities Accounts Payables 4, Capital and liabilities 64,

Financial Statements

There are two key elements to the financial statements of a sole trader business:

Statement of Financial Position – showing the financial position of a business at a point in time.

Statement of Profit or Loss – showing the financial performance of a business over a period of time.

The financial statements show the effects of business transactions.

We will use the duality concept – identifying the two sides of each transaction.

Example: T Smith - Sole Trader: Statement of Financial Position as at 31 December 2021

Non-current assets € € Motor car/Land and buildings/premises xxxx

Current assets Inventory xxxx Accounts Receivables xxxx Prepayments xxx Cash at bank xxxx Cash in hand xxxx xxxx Total Assets xxxx

Capital and Liabilities Capital xxxx Add: Net profit for year xxxx Less: Drawings (xxx) xxxx

Non-current liabilities Long-term Loan xxxx Current liabilities Accruals xx Accounts Payables xxxx xxxx Capital and Liabilities xxxx

T Smith - Sole Trader: Statement of Profit or Loss for year ended 31 December 2021

€ €

Sales revenue xxxx Cost of sales:

Accounting equation - tutorial

Course: Account (AA101)

University: Kolej Poly-Tech MARA BANGI