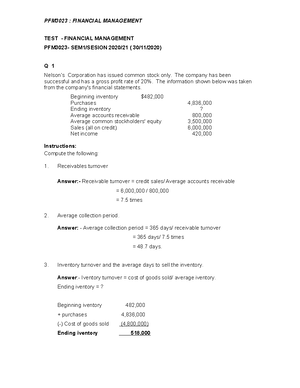

- Information

- AI Chat

Tutorial EPS 2 - Tuturial EPS chapter 2 yang sangat membantu kepada sesiapa yang tak tahu buat

Account (AA101)

Kolej Poly-Tech MARA BANGI

Recommended for you

Preview text

EPS/JAN 2018/FAR

QUESTION 1

Simple Delicacies Bhd is a well-established entity listed in Bursa Malaysia since 2010. The following are the information available during the year ended 31 December 2015 and 31 December 2016.

31 December 2015

Particulars RM Units Ordinary shares @ RM1 each 1,500, 0

1,500,

0

5% Non-cumulative preference shares @ RM0 each 2,000, 0

4,000,

0

EPS 2012 1.

EPS 2013 1.

EPS 2014 1.

EPS 2015 1.

31 December 2016

Particulars RM Units Ordinary shares @ RM0 each?? 5% Non-cumulative preference shares @ RM0 each 2,000, 0

4,000,

0

Net profit attributable to ordinary shareholders 2,500, 0

-

Additional information:

On 1 March 2016, the board of directors decided to issue a rights to purchase ordinary shares at lower than market price. The price agreed for the rights issue was RM1 per unit for every 4 shares held. The market price before the right issue was RM2 per unit.

The board of directors also agreed in a recent meeting dated 1 December 2016 to split each ordinary shares into 2 shares at a par value of RM0 each.

Required:

a. Explain potential ordinary shares in the context of MFRS 133: Earnings Per Share. Gives TWO (2) examples. (5 marks)

b. Compute the company’s basic EPS for the year ended 2016. Restate the comparative basic EPS if necessary. (6 marks)

c. Comment on the performance of the company based on EPS trends given and calculated above. (4 marks)

Suggested solution Question 1 a. In the context of MFRS 133, explain potential ordinary shares.

A potential ordinary share is a financial instrument or other contract that may entitle its holder to ordinary shares in the future. Examples would be:

a. financial liabilities or equity instruments, including preference shares, that are convertible into ordinary shares;

b. options and warrants;

c. shares that would be issued upon the satisfaction of conditions resulting from contractual arrangements, such as the purchase of a business or other assets,rights granted under employee share schemes.

(5 x 1 = 5 marks) b. Compute the company’s basic and diluted EPS for the year ended 2016. Restate the

comparative basic EPS if necessary.

EPS 2016

EPS (2016) = 2,500,

3,651,316of = RM 0 ~ RM0.

Net profit attributable to OSH

RM 2,500,

WANOS (2016)

1 January Balance bf

1,500,000 x 2/12 x 2/1 x 2/1 526,

1 March (right issue 1:4)

375,

1,875,000 x 9/12 x 2/1 2,812, 0 1 December (share split 1:2)

1,875,

x 2/ 31 December Balance cf

3,750,000 x 1/12 312,

WANOS 3,651, 6

Right issue TERP 4 shares @RM2 = 8. 1 share @RM1 = 1. 5 shares = 9. TERP = 9/ = RM1. Bonus factor 2/1.

Restatement of BEPS for prior year: EPS 2015 1 x ½ = 0.

EPS/JUN 2018/FAR

QUESTION 1

Mayabella Berhad (MB), a local manufacturing entity, was established in January 2015. It made up its first set of accounts to 31 December 2015 and continues to prepare its accounts to 31 December every year. On 1 January 2017, the issued share capital of MB comprises 10 million ordinary shares of RM1 each and 2 million 5% preference shares of RM1 each.

The following transactions occurred during the year of assessment 2017:

i. On 1 January, MB issued 5 million 10% convertible debentures. The debentures can be converted into ordinary shares in the ratio of 150 ordinary shares for every RM100 debentures.

ii. On 1 July, a rights issue of 1 for every 10 ordinary shares was made at RM2. each. The market value of the entity’s ordinary shares immediately before the right’s offer was RM3.

iii. 1 million ordinary shares of RM1 each were issued on 1 October. The shares were fully subscribed and paid upon its issuance.

Additional information:

a. Profit after tax for the year ended 31 December 2017 was RM12,000,000.

b. Mayabella Berhad paid preference dividend for half year only.

c. Tax rate is 24%.

d. Basic EPS and diluted EPS for year 2016 were RM1 and RM0 respectively.

Required:

a. Calculate the basic earnings per share to be reported in the financial statements of Mayabella Berhad for the year ended 31 December 2017, in accordance with the requirements of MFRS 133 Earnings Per Share. Restatement of Basic EPS is not required. (5 marks)

b. Calculate the diluted earnings per share for the year ended 31 December 2017, in accordance with the requirements of MFRS 133 Earnings Per Share. Show all workings. (6 marks)

c. Advise Mayabella Berhad on the steps needed to be taken in order to calculate the DEPS if it has more than one potential ordinary share. (4 marks)

EPS/JUL 2017/FAR

QUESTION 1

Kayaman Bhd has RM20 million issued and fully paid ordinary shares at RM1 per share as at 1 January 2016. The financial year end of the entity is on 31 December each year. The following information was available:

On 1 April 2016, the entity made a rights issue of 1 for every 4 shares. The rights issue was given to existing shareholders at RM1 per share when the market value was RM2. The market price prior to the rights issue was RM1 per share.

Immediately 3 months after the rights issue, the entity made a bonus issue of 1 for every 4 shares held.

On 1 September 2016, the entity issued RM2 million 10% debentures. The debentures are convertible into ordinary shares on the basis of 200 shares per RM100 debentures. None of the convertible debentures were converted as at 31 December 2016.

Net profit after tax for the year ended 31 December 2016 was RM5 million.

Assume the tax rate for 2016 is 25%.

Required:

a. Compute the basic earnings per share for Kayaman Bhd for the year ended 31 December 2016.

Restatement of comparative figures is not required.. (5 marks)

b. Compute the diluted earnings per share for the year ended 31 December 2016.

(6 marks)

c. Evaluate the effect on the diluted EPS for 2016 if on 1 November 2016 the entity has also offered a share options to the executives’ personnel to acquire 5 million shares at RM1 per share where the average price of an ordinary shares for the year was RM2. (4 marks)

Tutorial EPS 2 - Tuturial EPS chapter 2 yang sangat membantu kepada sesiapa yang tak tahu buat

Course: Account (AA101)

University: Kolej Poly-Tech MARA BANGI