- Information

- AI Chat

AUD339 Workbook for student

Auditing (AUD339)

Universiti Teknologi MARA

Recommended for you

Preview text

TEACHING AND LEARNING MODULE

FACULTY OF ACCOUNTANCY

AUD

AUDITING

MAIZURA MEOR ZAWAWI

ROSLAN ABD WAHAB

MOHD ZULFIKRI ABD RASHID

AMIZAHANUM ADAM

February 2020

TOPIC 1

INTRODUCTION

(TEST 1)

TOPIC COVERAGE

Introduction 1) Definition of auditing 2) Objectives of financial statements audit 3) Distinction between auditing and accounting 4) Management and auditor’s responsibilities 5) Demand for auditing 6) Types of audits a. Financial statement audit b. Compliance audit c. Operational audit d. Forensic audit 7) Types of auditors a. Chartered accountants b. Internal auditors c. Auditor-General d. Forensic auditors 8) Chartered accounting firms a. Structure of the firms b. Professional services Assurance services Non-assurance services

1) DEFINITION OF AUDITING

Definition 1 “Auditing is a systematic process of objectively obtaining and evaluating evidence regarding assertions about economic actions and events to ascertain the degree of correspondence between those assertions and established criteria and communicating the results to interested users.” (source: American Accounting Association Committee on Basic Auditing Concepts (1973, p. 8) Keywords Systematic process : audits are structured activities that follow a logical sequence Objectively : a quality methods by which information is obtained and also a quality of the person doing audit.(unbiased) Obtaining and evaluating evidence : a matter of examining the underlying support for assertions or representations Assertions about economic actions & events : An assertion is essentially a proposition that can be proved or disproved.(representations made by a responsible party in an accountability arrangement that pertains to economic actions and events) Degree of correspondence.. criteria: an audit establishes the conformity of assertions with specified criteria.

REASON FOR AUDIT OF COMPANY

The audit of company is a statutory requirement under Companies Act 2016 To increase the confidence level of the shareholders To reduce information risk i. risk that information provided is misleading / inaccurate. Helps owners assess how well managers have discharged their stewardship duties.

2) OBJECTIVES OF FINANCIAL STATEMENTS AUDIT

(a) To obtain reasonable assurance about whether the financial report as a whole is free from material misstatement , whether due to fraud or error, thereby enabling the auditor to express an opinion on whether the financial report is prepared, in all material respects, in accordance with an applicable financial reporting framework; and

(b) To report on the financial statements, and communicate as required by the Auditing Standards (ISAs), and in accordance with the auditor’s findings. The phrases used to express the auditor’s opinion are “ give true and fair view ” or “ present fairly, in all material respects ,” which are equivalent terms.

Both terms indicate financial statement are actually free from material misstatement.

Auditor needs to obtain a degree of reasonable assurance that the accounting & other records are not affected by material misstatements resulting from fraud & error.

Materiality – information is material if its omission or misstatement could influence the economic decision of users taken on the basis of the financial statements

Misstatement – a mistake in financial information which would arise from errors and fraud.

A misstatement in the financial statements can be considered material if knowledge of the misstatement would affects a decision of a reasonable user of the statements

Meaning of “TRUE AND FAIR VIEW”

True and Fair View is a legal concept but there is no legal definition made by the court. The decisions of courts are available only based on the concept in action

Basically, to be true, account must be in accordance with facts and reality. Fair is interpreted to mean that the accounts should be unbiased, just and equitable.

The accounts will be true and fair when the information they contain is sufficient in quantity and quality to satisfy the reasonable expectation of the readers to whom they are addressed

The court will treat compliance with the generally accepted accounting principles (GAAP) as reflected in the Statements of Accounting Standard as prima facie

SCOPE OF FINANCIAL STATEMENT AUDIT

The scope of Financial Statement audit is governed by:

Legislation Companies Act 2016 gives auditors the right to access the accounts & other records deemed necessary, thus unlawful if client impose restriction on any records or withholds info.

Regulations - Banks & Finance .companies incorporated under Companies .Act 2016 but activities monitored by the Bank Negara Malaysia (BNM). - Other regulations pertaining to type of industries

Auditing Standards International Standard on Auditing (ISA) & Malaysian Standard on Auditing (MASA)

3) DISTINCTION BETWEEN AUDITING AND ACCOUNTING

Auditing Accounting

Determine whether recorded info fairly reflects actual transactions

Record transactions & provide financial information

Auditor responsible to evaluate the system to determine its effectiveness

Accountant responsible to develop a system to ensure that transactions are properly recorded

Auditor must understand accounting principles so that he/she would be able to detect non-compliance by the Accountant

Accountant must understand accounting principles so that transactions were recorded according to accepted standards

Auditor should possess expertise to accumulate & interpret audit evidence

Accountant should possess expertise to record transactions & to prepare financial statements

4) MANAGEMENT AND AUDITOR’S RESPONSIBILITIES

MANAGEMENT’S RESPONSIBILITY

Preparation of yearly financial statements To develop and maintain adequate accounting records and internal control systems Safeguarding of company’s assets Prevention and detection of errors, irregularities & fraud

AUDITOR’S RESPONSIBILITIES

To state an opinion on the financial statements in auditor’s report based on his independent examination. AI 200 also noted that: An audit in accordance with ISAs/MASA is designed to provide reasonable assurance that the financial statements taken as whole are free from material misstatements To report on the effectiveness of internal control over financial reporting To identify material weaknesses in internal control and provide recommendations to overcome weaknesses (letter of weaknesses / management letter) To perform audit with due care and professional competence. To conduct audit with professional scepticism i with questioning mind and critical evaluation of evidence

Reasonable assurance are:

measure of the level of uncertainty that the auditor has obtained at the completion of the audit Reasonable but not absolute, indicates that the auditor is not insurer or guarantor of the correctness of the FS Reason for stating reasonable assurance: 1. Audit evidence resulted from testing a sample of population 2. Accounting presentations contain complex estimates 3. Fraudulent are often difficult to detect

AUDITOR’S RESPONSIBILITIES FOR DETECTING & REPORTING OF FRAUD &

ERROR

AI 240 Fraud & Error What is a fraud? Fraud : Intentional misrepresentations of financial information by 1 or more individuals among management / employee or 3rd parties, involving: 1. Manipulation, falsification or alteration of records or documents 2. Misappropriation of assets 3. Suppression/omission of the effects of transactions from records/documents 4. Recording of transactions without substance 5. Misapplication of accounting policies

Error : unintentional mistakes in financial information such as; 1. Mathematical or clerical mistakes in the underlying records and accounting data 2. Oversight or misinterpretation of facts, or 3. Misapplication of accounting policies

WHO ARE RESPONSIBLE TO DETECT FRAUD & ERROR? MANAGEMENT OR AUDITOR?

Management

Responsible to prevent & detect F & E through the implementation & continued operation of an adequate system of IC. H/over such system will only reduce, not eliminating the possibility of F & E Plan audit so that they would have reasonable expectation of detecting

shareholders when required adjustments are not made.

DEMAND FOR AUDITORS’ SERVICES

g Relationship of External User to Management and Independent Auditor Attest Function

Financial report for external users

External users Conflict of interest Prepare Shareholders Separation between Management Bankers Owners (shareholders) responsible for Government agencies and management accuracy and Potential shareholders adequacy of Creditors Financial reports Suppliers Employees Need for protection of absentee owners

Credibility gap

Need for assurance as to reliability of financial report

Assurance provided by independent auditor

6) TYPES OF AUDITS

TYPES PURPOSE PERFORMED BY

FINANCIAL

STATEMENT AUDIT

To determine whether FS reflects true & fair view, according to accounting standards & Company Act 2016

- Approved Company Auditor/External Auditor

- Government Auditor

OPERATIONAL

AUDIT

To evaluate effectiveness & efficiency of operating/Procedures

- Internal auditor

- Government Auditor

COMPLIANCE

AUDIT

To determine whether specific procedures/rules & regulations were being complied with

- Internal auditor

- Government Auditor

FORENSIC AUDIT To detect/ deter fraudulent activities

- Forensic auditor

DIFFERENCES BETWEEN INTERNAL AUDITING & EXTERNAL AUDITING

Characteristics Internal Auditing External Auditing

Performance/ Status

By employee within the organization/company

By practising professional outside the organization/Chartered Accounting Firm

Primary concern To serve the needs of the organization

To serve the needs of third parties, eg: shareholders

Objective of review To develop improvements & induce compliance with established policies & procedures

To determine reliability of Financial Reports

Independence Independence organizationally but ready to respond to needs & desires of management

Independence in fact and appearance

Detection of fraud Directly concerned with prevention & detection of fraud

Incidentally concerned with prevention & detection of fraud

Period/Frequency Continuous review/throughout the year or as requested by management

Periodic evaluation/financial year ended

Scope of audit Determined by the management Laid by the Statutory

Appointment Appointed by the company’s management through formal interview process

Appointed by the company’s shareholders through voting at AGM (or other types of appointment as per Companies Act 2016)

Salary/remuneratio n

Salary; fixed internally Agreed by the auditors & management ; as per Companies Act 2016

Reporting Responsibility

To the board of directors or to the audit committee or to the management

To the company’s shareholders

Rights and duties Defined by company’s As laid down by Companies

management Act 2016

DEVELOPMENTS IN MALAYSIA

The Malaysian Institute of Accountants (MIA)

The Malaysian Institute of Certified Public Accountants (MICPA)

- Regulatory Body , established by Accountants Act 1967

Business managed by council members

Issue auditing standards and Code of ethics

Does not conduct professional exams

Formed in 1958

A professional body

Managed by Council elected by members

Conducts professional exams

INFLUENCES ON THE DEVELOPMENT OF AUDITING

International Federation of Accountants (IFAC)

Develops and implements international auditing standards. The International Statement of Auditing (ISA) and International Statement of Quality Control (ISQC) are adopted and used by most jurisdictions including Malaysia

The Quality Standards recommended by IFAC includes the following: having audit policies and a methodology for conducting transnational audits in accordance with International Standards of Auditing

complying with the IFAC Code of Ethics

maintaining training programmes to keep partners and staff up to date on international developments in financial reporting

maintaining quality control standards and conducting regular quality assurance reviews to monitor compliance with the firm’s policies and methodology

Other regulatory requirements ;

Companies Act 2016

Securities Commission Act

Capital Market and Services Act

Bursa Malaysia requirements

MIA by laws

BODIES RELATING TO AUDITING IN MALAYSIA

Malaysian Institute of Accontants (MIA) National acc body, est. under Accountants Act 1967

Member of IFAC, adopts ISAs as the basis for developing stds & issuing pronouncements on auditing matters

INTRODUCTION TO AUDITING STANDARDS

The council of the Malaysian Institute of Accountants (MIA) has determined that approved Auditing Standards for members comprise:

International Standards on Auditing (ISA) issued by the International Auditing Practices Committee (IAPC) of the International Federation of Accountants (IFAC) and approved by the MIA

Malaysia Approved Standards on Auditing (MASA) issued by the MIA

IAPC believes the issue of such standards will help improve the degree of uniformity of auditing practices throughout the world.

MASA are produced and issued by the Malaysian Institute of Accountants (MIA) as parts of its effort to define standards of auditing and harmonise auditing practices in Malaysia and are intended to cover topics not dealt within an ISA or topics where particular features of the Malaysian environment warrant a domestic standard.

In addition to these promulgated standards, Auditing Technical Release and other statements issued by the Council relating to auditing are to be regarded as opinions on best current practice and thus form part of Generally Accepted Auditing Principles (GAAP)

COMPLIANCE WITH APPROVED AUDITING STANDARDS Independent auditors are required to use approved Auditing Standards in the conduct of their audits

Audit reports should contain a positive statement to the effect that the audit has been conducted in accordance with approved Auditing Standards

8) CHARTERED ACCOUNTING FIRMS

a. Structure of the firms

Continuing Professional Development

b. Professional services

Auditing & Assurance Services

Financial Statement Audit

Other Audit & Assurance Services

Compliance Audit Operational Audit Forensic Audit

Related Services (Non-assurance Services)

Management Advisory Services Accounting & Compilation Services

EXERCISES

Definition of Auditing “Auditing is a _____________________________ of ____________ obtaining and _________ evidence regarding __________ about economic actions and events to ascertain the _____________ of _______________between those assertions and established criteria and _________________ the results to interested ____________.” (source: American Accounting Association Committee on Basic Auditing Concepts (1973, p. 8)

Objective of Audit

To obtain _____________ _______________ about whether the financial statements as a whole are ______ from __________ _______________, whether due to _______or ________, thereby enabling the auditor to express an opinion on whether the financial statements are prepared, in all material respects, in accordance with an applicable financial reporting framework; and

b Compliance audit

c Operational audit

d Forensic audit

- Types Of Auditors

Types of auditors Explanation

a Chartered accountants

b Internal auditors

c Auditor General/Government Auditors

d Forensic auditor

TOPIC 2

AUDIT REGULATION

TOPIC COVERAGE

Companies Act 2016 Sec. 261 : Auditor’s statement Sec. 263 : Company Auditors Sec. 264 : Company auditors (Disqualification) Sec. 266 (1) – (3) : Duties of auditors Sec. 266 (4) – (7) : Powers of auditors Sec. 267 : Appointment of auditors of private company Sec. 271 : Appointment of auditors of public company Sec. 274 : Fixing of auditor’s remuneration Sec. 281 : Resignation of auditors Sec. 282 : Notice of resignation of auditor to Registrar Sec. 283 : Rights of resigning auditor of a public company Sec. 276 : Resolution to remove auditor from office Sec. 277 : Special notice required for resolution to remove auditor from office

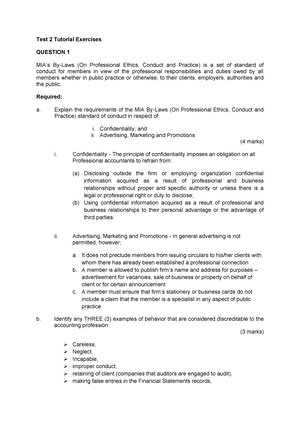

MIA’s By-Laws (On Professional Ethics, Conduct and Practice) Part I:By-Laws on Professional Ethics Part A:General Application o 100Fundamental principles and conceptual framework 110 Integrity 120 Objectivity 130 Professional competence and due care 140 Confidentiality 150 Professional behavior 150 Advertising, marketing and promotions 100 Threats and safeguards o 290 Independence o 500 Method of Practice o 240 Audit Fees o 240 Commission o 240 Referral

Standards on auditing International Standards on Auditing Malaysian Approved Standards on Auditing

AUD339 Workbook for student

Course: Auditing (AUD339)

University: Universiti Teknologi MARA

This is a preview

Access to all documents

Get Unlimited Downloads

Improve your grades