- Information

- AI Chat

AUD589 SOLUTION PAST YEAR GOOD FOR YOU TO REFER

Auditing (AUD339)

Universiti Teknologi MARA

Recommended for you

Preview text

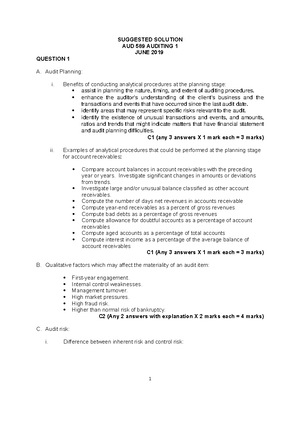

SUGGESTED SOLUTION – AUD 589

JUNE 2018

QUESTION 1

a. Purposes of audit planning: To devote appropriate attention to important areas of the audit. To identify and resolve potential problems on a timely basis. To effectively and efficiently organize and manage the audit engagement. To select engagement team members with appropriate levels of capabilities and competence. To direct and supervise engagement team members. To coordinate work to be done among the engagement team members. To assist in the review of the findings by the engagement team members. (Any 6 purposes x 1 mark each = 6 marks)

b. Benefits of conducting ratio analysis for the analytical procedures: Ratio analysis makes it easy to grasp the relationship between various items and helps in understanding the financial statements. Ratio analysis establishes the numerical or quantitative relationship between two figures of a financial statement to ascertain strengths and weaknesses of the company as well as its current financial position and historical performance. Ratio analysis helps the auditors to make an evaluation of certain aspect of a firm’s performance and going concern prospect. (Any 2 with explanation x 2 marks each = 4 marks)

c. Risks of material misstatements noted from the conversation: Lack of training during the two hours on operating the sales system could lead to error. o Lead to errors in the initial setting-up of the menu and prices. o Employees not trained by the vendor, but trained by the two employees, might make errors when using the system. Lack of accounting skills and segregation of duties. o Account executive just recently appointed hence could lead to errors in recording, since not familiar with the accounting system. o Incompatible duties, authorization, record keeping and physical custody are done by one person. The company operations are subject to regulations (JAKIM’s halal certification). o Non-compliance with the regulation could result in litigations. o Company might have to temporarily close the business and this could result in writing off of spoilt perishable goods. The company depends on foreign kitchen workers on contract basis. o Poor retention rates, might affect the completeness payroll registers. o Attendance and overtime need to be closely monitored and approved in order to avoid fraudulent claims. The cash are kept overnight for protection.

o If the cash are not physically safeguarded, then they can be stolen, damaged or misplaced. o Company might require to write off the cash receipts and accounts receivable for the stolen, damaged or misplaced cash. (Any 5 with explanation x 2 marks each = 10 marks) (Total: 20 marks)

QUESTION 2

A. Characteristics of good audit documentation: Each audit file should be properly identified with such information as the client’s name, period covered, a description on contents, initials of preparer, date of preparation and an index code. Audit documentation should be indexed and cross-referenced to aid in organizing and filing. Completed audit documentation must clearly indicate the work performed. E. notations on each schedule used. Audit documentation should include sufficient information to fulfill the objectives for which it was designed. The conclusions that were reached about the segment of the audit should be plainly stated in the audit documentation. (Any 4 with explanation x 2 marks each = 8 marks)

B. Two factors that may affect reliability of external confirmations: The form of the confirmation Prior experience with the entity The nature of the information being confirmed The intended respondent (Any 2 with explanation x 2 marks each = 4 marks)

C. a. Audit procedures for inventory: Observe the physical inventory stock count Examine the receiving and issuing activity Perform cut – off analysis Perform analytical procedure i. computation of related ratios Reconcile inventory count to inventory ledger (Any 2 with explanation x 2 marks each = 4 marks)

b. The importance of auditor’s attendance during physical inventory stocktaking: Attendance at stocktaking can provide evidence to the auditor in respect of the: Existence assertion Completeness assertion Valuation assertion Consideration of possible inventory obsolescence and deterioration (Any 2 with explanation x 2 marks each = 4 marks) (Total: 20 marks)

The particulars in the statement of account must match with the particulars in the accounts payable. The documents need to be checked for agreement. If there are discrepancies, then reconciliation needs to be done. The possibility of reconciling items could be for those items due to the timing differences between the date of payment and the date of bank-in by the suppliers. Any other acceptable answers. (Any 3 with explanation x 3 marks each = 9 marks) (Total: 20 marks)

QUESTION 4

A. a. Imprest petty cash fund is commonly used to pay for small, routine and incidental expenses. This account has a fixed debit balance, which is replenished should the balance fall below certain amount. (2 marks)

b. Objective of testing bank reconciliation statement: To substantiate that the balance of client’s bank/cash book agree with the bank statement. To determine adjusting entries to reconcile two sets of records for cash/bank transactions. (Any 1 with explanation X 1 marks = 3 marks)

c. Audit procedures that can be performed for cash and bank balances: Confirm bank balances Verified bank reconciliation Counting cash on hand Performed cut off bank statement (Any 3 with explanation x 2 marks each = 6 marks)

B a. Importance of maintaining a proper property, plant and equipment register:

Assists in both short and long term planning: A well-prepared PPE register

presents a valuable planning tool to any business. This helps the

company to keep track of details of each PPE, including their date of

purchase and risk assessment.

Helps in preventing fraud: Companies should have their PPE audited

regularly to check that the internal accounting control systems are

accurately reflecting the company’s PPE position. When there are

accurate controls in place, asset theft and the opportunity to lose assets at

service providers, customer sites etc. reduces significantly.

Helps keep things organised: By tracking the movement of PPE, a

business can optimise the utilisation of their PPE including increased

billings. With a PPE register in place, an organisation’s assets become

safeguarded from any threats that would impact the business’ ability to

maximise revenue.

Saves cost: A PPE register presents many cost saving opportunities for

most businesses. By understanding what assets you have on hand, this

will prevent duplication of asset purchases thus improving cash flow and

profitability.

(Any 2 with explanation x 2 marks = 4 marks)

c.

(1 Analytical review procedures used in auditing property, plant and equipment: Compare prior-year balances in PPE and depreciation charges with current year balances after consideration of any changes in the asset’s condition. Compute the ratio of depreciation charges to the related PPE. Compute the ratio of repair & maintenance expenses related to PPE. Compute the ratio of insurance expense to the related PPE. Review capital budget and comparison of the amount spent with amount budgeted for PPE. (Any 2 with explanation x 2 marks each = 5 marks) (Total: 20 marks)

QUESTION 5

A. 1. The auditor should issue an audit report with a (qualified or disclaimer opinion) in view that the auditors are restricted from performing the audit procedures and the account receivables are potentially major customer of which any complaint from these customers could lead to the company losing a material amount of sales/assets.

The auditor should issue an audit report with a (qualified or adverse opinion) since the applicable financial reporting framework such as IFRSs, requires including a statement of cash flows among the financial statements. The auditor is not required to prepare the statement of cash flows for disclosure in the audit report.

If the information in the management report is not revised, the auditor should issue an (emphasis of matter report describing the material inconsistency) in the management report.

Orochimaru Bhd’s financial performance is not strong enough as being reflected by net liabilities position and net loss result. It might not be able to continue its operation without disruption if it keeps on showing poor performance. This will definitely raise substantial doubt that the company can continue as a going concern. Thus, modified report with emphasis of matter paragraph should be issued to draw attention on the going concern issues in the notes. (1 mark for type of audit report + 1 mark for justification = 8 marks)

B. a. The significance of the following basic elements of the audit report is: i. Report title - the audit report should be appropriately titled so that it is clear to the user that the financial statements have been audited. The title will also distinguish the auditors’ report from reports for non-audit engagements and other statements contained in the annual report such as the directors’ report or the chairman’s statement.

AUD589 SOLUTION PAST YEAR GOOD FOR YOU TO REFER

Course: Auditing (AUD339)

University: Universiti Teknologi MARA