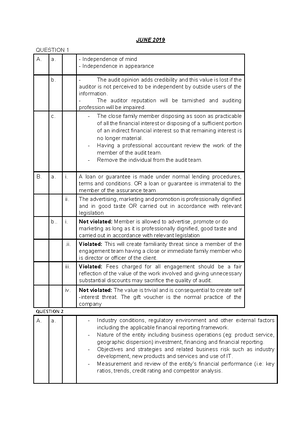

- Information

- AI Chat

Audit Evidence - All the best

Auditing (AUD339)

Universiti Teknologi MARA

Recommended for you

Related Studylists

AUD SS FEPreview text

AUDIT EVIDENCE AND AUDIT DOCUMENTATION

Audit Evidence ▪ The information used by the auditor in arriving at the conclusions by which the auditor’s opinion is based. ▪ Sources of audit evidence: ➢ Obtained directly by the auditor ➢ From the management ➢ From third party

Persuasiveness of Evidence ▪ Persuasiveness of evidence depends on: 1. Sufficiency – The quantity of evidence (in the form of samples selected for test), whether it is adequate to achieve the audit objective.

- Appropriateness – The quality of evidence, whether it is suitable to meet the audit objective.

Pop quiz: If the audit obj is to determine whether the MV purchased during the year exists or not, which of the following audit procedures is deemed as appropriate? 1. Examine the supporting documents for the purchase of MV. 2. Physically examine a sample of motor vehicles purchased during the year.

❑ Relevance – The appropriateness & suitability of the evidence to the audit objective that the auditor is testing.

❑ Reliability – The degree to which evidence can be considered believable or worthy of trust.

Characteristics of reliable information a. Independence of provider – Evidence obtained from external source is more reliable than the one obtained from internal source. E., confirmations obtained from client’s banks or debtors are more reliable than documents obtained from the client. b. Effectiveness of client’s internal control – Evidence is more reliable if the client’s internal control system is effective. c. Auditor’s direct knowledge – Evidence obtained directly by the auditor through physical examination, observation, computation and inspection is more reliable than information obtained indirectly. d. Qualifications of individuals providing the information – Evidence is more reliable if it is obtained from a qualified person. e. Degree of objectivity – Objective evidence is more reliable than evidence that requires considerable judgement.

❑ Timeliness – The timing in obtaining the evidence. Refer to when the evidence was accumulated and the period covered by the audit. E., 1) Evidence for assets, liabilities or equity is more persuasive if it is closer to the date of SOFP. 2) Evidence for revenues and expenses is more persuasive if it covers the entire period under audit.

Types of Audit Evidence 1. Physical examination @ Inspection of tangible assets – inspection or count of tangible asset. e., count petty cash on hand; verify the amount of closing inventories, verify the machinery & equipment, examine the furniture.

- Documentation @ Inspection of records or documents – examination of client’s documents and records to substantiate the information that is or should be included in financial statements. e., examine supplier’s invoices; examine the payment voucher, examine bank statements, examine the land title

▪ Two categories of documentation:

a. Internal documents: Document prepared and used within an organisation without ever going to an outside party (such as customer or vendor). E., punch card, duplicate sales invoice, copy of official receipt, journal, internal report.

b. External documents: Document either originated by an outside party or internal document that went to an outside party. E., supplier’s invoice, bank statement, validated deposit slip.

▪ External documents are regarded as more reliable than internal ones since the former (external documents) have been in the hands of both the client and external party to the transaction, thus indicating that both parties are in agreement about the information stated in the document.

Observation – the use of the senses to evaluate certain activities. E., observe the handling of cash by our client; observe whether store room housing valuable inventories were always locked.

Confirmation – receipt of written or oral response directly from an independent third party verifying the accuracy of information requested. E., confirm client’s cash balance with bank; confirm account receivable balances with the debtor, confirm legal obligation of the client with the lawyers.

Types of Confirmation Letter:

i. Positive CL: The third party is requested to confirm (reply) directly to the auditor of whether the balance is correct or not.

ii. Negative CL: The third party is requested to confirm (reply) directly to the auditor only if the balance is incorrect. IOW, the third party does not have to reply if the balance is correct.

Audit documentation (Working papers)

Working papers are records prepared or obtained by the auditor in connection with the audit.

Purpose of working papers: a. to provide a basis for planning current year audit (e., by making reference to previous year’s time budget, internal control system etc). b. to provide a record of evidences accumulated. c. to provide data for deciding the proper type of auditor’s opinion. d. to provide basis for review by partner and supervisor (in order to maintain the quality of the audit).

Types of audit working paper files:

▪ Permanent files: Auditor’s working paper file that contain data of continuing importance from one year to another. E., copies of MA & AA, contracts, loan agreement, information pertaining to client’s internal control system (such as flowcharts, internal control questionaires), organisation chart, address of registered offices.

▪ Current files: Auditor’s working paper file that contain data applicable to the current year under audit. E., audit programmes, documentation of audit evidence, minutes of directors’ meeting, a copy of financial statements, ratio analyses.

Working papers: ➢ are owned by the auditors and are retained at the Auditor’s premises after completion of an audit. ➢ can be used by the client if the auditor wants to release them after a careful consideration of whether there might be confidential information in them. ➢ Can be subpoenaed by a court and thereby becomes property of the court. ➢ Can be released to other users only if the auditor obtains permission from the client.

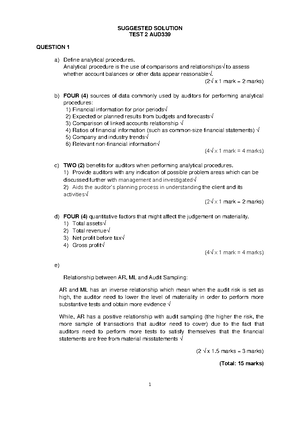

Pop Quiz: Explain briefly the advantages of Analytical Procedures (AP):

AP enables the auditor to reduce the cost of an audit since the unnecessary audit procedures could be avoided (If the account balances appear reasonable, the audit procedures could be reduced).

AP enables the auditor to focus on high risk areas and perform a more detailed audit tests / extent the audit procedures on unreasonable account balances. Thus, AP helps the auditor in achieving an effective and efficient audit.

Audit Evidence - All the best

Course: Auditing (AUD339)

University: Universiti Teknologi MARA

![Chapter 1 Partnership, FAR 160 [Lecturer Notes]](https://d20ohkaloyme4g.cloudfront.net/img/document_thumbnails/1725fd64c6586cc441c660830d3a6800/thumb_300_388.png)