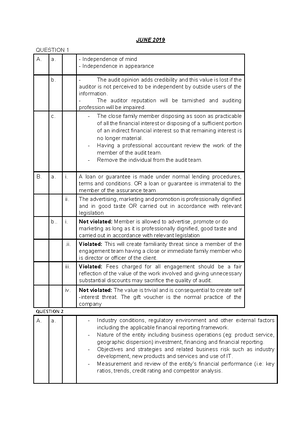

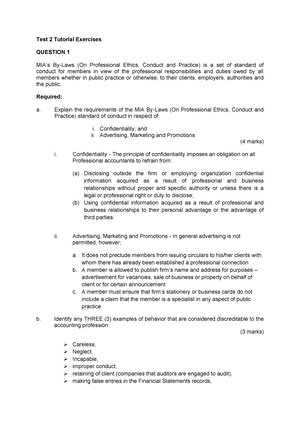

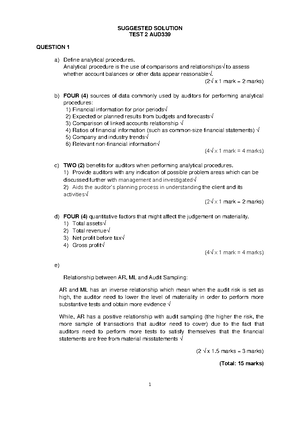

- Information

- AI Chat

Introduction to Auditing

Auditing (AUD339)

Universiti Teknologi MARA

Recommended for you

Related Studylists

AUD339Preview text

INTRODUCTION TO AUDITING

❖ Why audit is necessary? The agency relationship between the owners (shareholders) of a company and the management (board of directors) resulted in a conflict of interest (due to the information asymmetry between them). The management might be biased in presenting the financial information to the shareholders.

As such, the independent auditor plays an important role to safeguard the interest of the shareholders by reducing information risk (the risk of misleading information in the financial statements) through the issuance of an objective opinion (unbiased opinion) on the financial statements prepared by the management.

ACCOUNTING AUDITING

- Accountant is responsible for the maintenance of accounting records and preparation of financial statements.

Auditor is responsible for issuance of an objective opinion on whether the recorded information fairly reflects actual transactions. 2) Accountant is responsible to develop / design a good internal control system to ensure that transactions are properly recorded.

Auditor is responsible to evaluate the system to determine its effectiveness.

- Accountant must understand accounting principles so that transactions were recorded according to the accepted standards.

Auditor must understand accounting principles so that he/she would be able to detect non-compliance by the Accountant to the accounting standards. 4) Accountant should possess expertise to record transactions and to prepare financial statements.

Auditor should possess expertise to accumulate and interpret audit evidence.

❖ Types of Audit:

- Financial Statement Audit

- Purpose: To determine whether or not the financial statements reflect true and fair view of the company’s financial performance and position and whether the accounts were prepared based on approved reporting standards and provisions of the Companies Act.

- Nature: Highly standardised.

- Always performed by External Auditor (Chartered Accountant)

“AN INDEPENDENT AUDITOR SHOULD DETERMINE AND ISSUE AN OBJECTIVE / UNBIASED OPINION ON WHETHER THE FINANCIAL STATEMENTS REFLECT A TRUE & FAIR VIEW OR NOT”

Operational Audit

- Purpose: To evaluate effectiveness and efficiency of operating procedures/systems.

- Nature: Highly non-standardized and often subjective.

Compliance Audit

- Purpose: To determine whether specific procedures/rules & regulations were being complied with (followed or not).

- Nature: Non-standardized but specific and usually objective.

Forensic Audit

- Purpose: To investigate, detect or deter fraudulent activities

- Nature: Highly non-standardized, very subjective and sometimes sensitive

❑ Financial statements audit involve evaluation of evidence to support management assertions in the financial statements.

❑ Management Assertions: o Existence: Management asserts / claims that all the assets, liabilities and equities presented in the financial statements really exist.

o Rights and Obligations: Management claims that the company has a right over the assets and obligation to pay for the liabilities that are reported in the FS.

o Occurrence: The management claims that all business transactions reported during the financial year have really occurred / happened.

o Completeness: The management claims that all transactions and account balances have been reported completely (without omission)

o Valuation: The management claims that all assets and liabilities have been properly valued as at the cut-off date of the financial statements.

o Measurement: The management claims that the business transactions during the financial year have been properly measured.

o Presentation and Disclosure: The management claims that the business transactions and account balances have been properly presented and disclosed in accordance with the requirements within the financial reporting framework (such as IFRS, MFRS, MPERS).

❑ The financial statements reflect a true & fair view of an entity’s financial performance and financial position when: ▪ All important facts were disclosed in the FS ▪ Information in the FS was not misleading ▪ The FS are free from material misstatements ▪ The FS complied with the relevant Financial reporting standards

❑ Materiality ▪ The degree of importance of a particular item in the financial statements. An item is considered material if it would significantly affect decision making process of the user (reader). ▪ Immaterial = insignificant

❑ The auditor is not able to ensure accuracy / correctness of the FS because: ▪ He uses the sampling techniques whereby not all transactions would be selected for review. There might be a sampling risk i., the risk that the auditor might make a wrong conclusion when the selected samples do not represent the entire population of transactions.

▪ The FS always contain accounting estimates which are subject to error. Therefore, the auditor is not in a capacity to ensure accuracy or correctness of the figures stated in the FS.

❑ Major Services of Chartered Accountant Firms Assurance Services 1. Auditing & Assurance services: Issue written communication about reliability of certain information

Non-assurance Services 2. Accounting & bookkeeping: Prepare financial statements (acctg), Prepare journals & ledgers (bookkeeping) 3. Tax services: Prepare tax return and give advice on tax planning 4. Management advisory services: eg: Give advice on how to improve accounting system, developing office computer networks

❑ Acctg standards: IFRS, MFRS, MPERS

❑ Auditing standards: Malaysian Approved Standards on Auditing (MASA)

Auditing standards are guidelines for the performance of the audit so that the audit work would be performed systematically by using the appropriate procedures.

❖ Important terms: ▪ Independent ▪ Objective ▪ Unbiased ▪ Misstatement ▪ Assertion ▪ Audit opinion ▪ True & fair view of financial performance and financial position

❖ Important points: ▪ The management is responsible to prepare the FS. ▪ The management is responsible to ensure that the FS reflect a true & fair view. ▪ FS are not 100% accurate because of the accounting estimates used (Accounting estimates are based on professional judgement, which is subject to error and uncertainty). ▪ The term ‘True & Fair’ does not mean that the FS are 100% accurate. ▪ The auditor is not responsible to ensure accuracy of the FS. ▪ The auditor is only responsible to provide reasonable assurance (NOT absolute assurance and NOT a guarantee) / to give an opinion on whether the FS reflect a true & fair view or not. ▪ MFRS (standards for accounting & financial reporting) is different from MASA i., Malaysian Approved Standards on Auditing. MASA contains various guidelines & standards relating to the performance of the audit including audit planning, collection of evidence and issuance of the auditor’s opinion.

❖ Self-review questions (PLS PREPARE WRITTEN ANSWERS): ▪ What is the final product of a financial statements audit? ▪ Can the internal auditor be appointed to carry out financial statements audit? ▪ Can the auditor ensure accuracy of information contained in the financial statements? ▪ Can the auditor guarantee accuracy of information contained in the financial statements? ▪ Can the auditor guarantee that the financial statements reflect a true and fair view of the financial position? ▪ Why audit is important to the shareholders?

Introduction to Auditing

Course: Auditing (AUD339)

University: Universiti Teknologi MARA

![Chapter 1 Partnership, FAR 160 [Lecturer Notes]](https://d20ohkaloyme4g.cloudfront.net/img/document_thumbnails/1725fd64c6586cc441c660830d3a6800/thumb_300_388.png)