- Information

- AI Chat

TEST 2 AUD339 JAN2021 Q - test 2 for auditing subject

Auditing (AUD339)

Universiti Teknologi MARA

Recommended for you

Preview text

CONFIDENTIAL AC/JAN 2021/AUD

UNIVERSITI TEKNOLOGI MARA

TEST 2

COURSE : AUDITING

COURSE CODE : AUD

EXAMINATION : JANUARY 2021

TIME : 1 HOUR 30 MINUTES

INSTRUCTIONS TO CANDIDATES

This question paper consists of THREE (3) questions.

Please submit your HANDWRITTEN answers in ONE (1) pdf file only. Answers that are typed – in will not be accepted

Please rename your file to the following: (NAME_STUDENT ID_CLASS)

Answer ALL questions in English.

DO NOT TURN THIS PAGE UNTIL YOU ARE TOLD TO DO SO This examination paper consists of 4 printed pages

CONFIDENTIAL 2 AC/DEC 2019/AUD

Answer ALL Questions

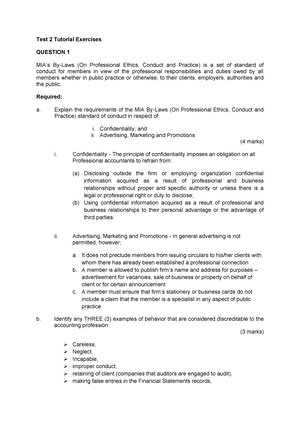

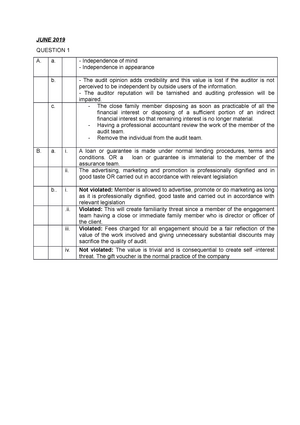

QUESTION 1

Audit planning is important for the audit to be completed in an efficient and effective manner. The auditor must consider to perform preliminary analytical procedures, the issues of relative risk and setting the materiality level in preparing the audit program.

Required:

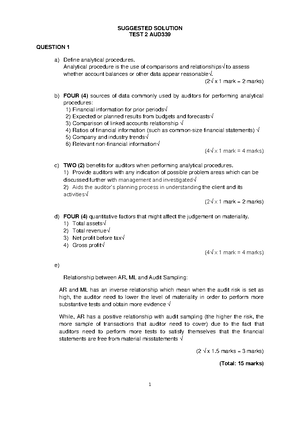

a. Describe THREE (3) benefits of analytical procedures in preliminary planning. (3 marks)

b. Give any THREE (3) examples of key ratios. (3 marks)

c. Define the term “materiality” under paragraph 3 ISA 320. (3 marks)

d. Explain why materiality is important but difficult to apply in practice. (3 marks)

e. Identify any THREE (3) examples of quantitative factors that might affect the preliminary judgement on materiality. (3 marks) (Total: 15 marks)

QUESTION 2

At the planning stage, it is important for the auditor to identify the risk factors that might affect the nature, extent and timing of further audit procedures to be performed. If the audit is not properly planned, the auditor may issue an incorrect audit report or conduct an inefficient audit.

Required:

a. State THREE (3) components of audit risk model. (3 marks)

b. Identify THREE (3) steps to minimize audit risk. (3 marks)

c. State the components of audit risk in each of the following circumstances:

i. Inspection of the company’s property, plant and equipment was not carried out due to time constraint. ii. The company sold most of its products on cash basis to retail customers. iii. The company’s inventories are subjected to technological obsolescence. iv. A small company could not implement segregation of duties due to limited staff. v. Purchase of office stationeries were not approved by any of officers. (5 marks)

CONFIDENTIAL 4 AC/DEC 2019/AUD

B. In the audit of cash, an auditor should be able to differentiate between verifying the client’s reconciliation of the balance on the bank statement to the balance in the general ledger, and verifying whether recorded cash in the general ledger correctly reflects all cash transactions that took place during the year.

Required:

a. Explain a reason the need for a significant amount of time in verifying cash balances. (2 marks)

b. Identify the specific audit objectives for the following audit procedures in verifying the cash account. i. Review the financial statements to make sure that bank overdrafts are recorded as current liabilities. ii. Count the cash in hand on the last day of the year and subsequently trace them to deposits in transit and the cash receipt journal. iii. Prove the bank reconciliation as to additions and subtractions, including all reconciling items. iv. Trace the cash book balance on the reconciliation to the general ledger. (4 marks)

c. State any FOUR (4) substantive audit procedures for verifying cash in hand. (4 marks) (Total: 20 marks

GRAND TOTAL: 50 MARKS

END OF QUESTION PAPER

TEST 2 AUD339 JAN2021 Q - test 2 for auditing subject

Course: Auditing (AUD339)

University: Universiti Teknologi MARA