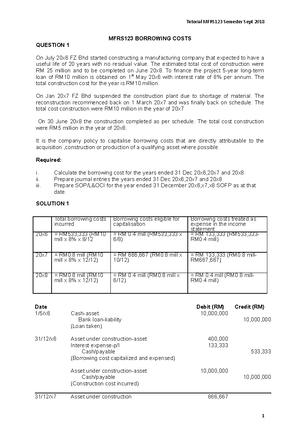

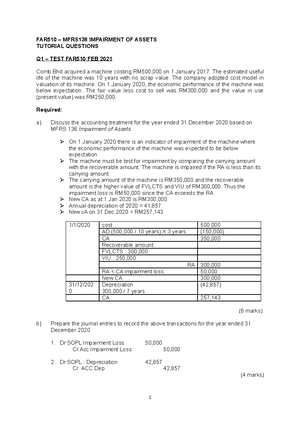

- Information

- AI Chat

Tips MIA By Law / its easy and catchy feel free to download

Auditing (AUD339)

Universiti Teknologi MARA

Recommended for you

Preview text

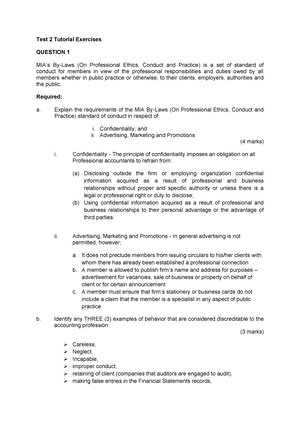

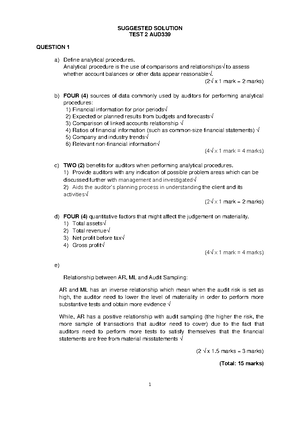

EXAMPLE OF QUESTIONS AND SUGGESTED REASONS

Reasons

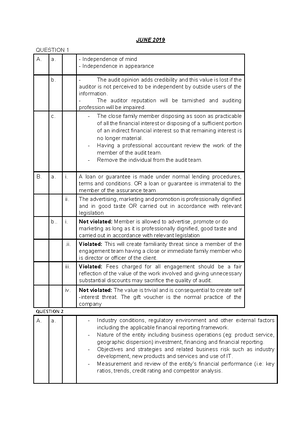

- Nazura provides accounting service since 3 years ago. Nazura recently appointed as auditor.

Violated. This may create a self-review threat. Nazura might be biased in issuing audit opinion

- Nazura disclosed certain confidential info to investigation committee of MIA without seek permission from Client

Not violated. Under confidentiality, auditor has professional duty to disclose such information without seeking permission 3. General manager of Mukmin Bhd wants Aryan, the audit partner in charge for Mukmin Bhd to help in preparing interim FS

Violated. This may create a self-review threat. Aryan might be biased in issuing audit opinion

- Aryan was offered 20 free tickets to Sunway Lagoon which worth RM4,000 in recognition of good work. Aryan accepted.

Violated. This may create a threat to independence/self-interest threat. Aryan might be biased in issuing audit opinion 5. Aryan found material misstatement of net income on previous year’s tax return. Management refused to take corrective action. Aryan informed IRB.

Not violated. Under confidentiality, auditor has a legal duty to disclose such information

- Mukmin Bhd traditionally gives hampers during festive seasons. This year, Aryan was sponsored with a family dinner worth RM3,000 in a 5-star hotel

Violated. This may create a self-threat due to acceptance of undue hospitality. Aryan might be biased in issuing audit opinion or the independence might be impaired 7 , Chartered Accountant has outstanding loan of RM110,000 from Setia Bhd. The loan is on normal lending policy and no special treatment was given to Rahim. Rahim & Chia accepted the appointment as external auditor of Setiaraya. Chia will be partner in charge

Not violated. There is no issue of independence as the outstanding loan is made under normal lending policy.

- Rahim & Chia provide accounting & tax services to Bahtera from 1.8 to 31.12. The management proposed Rahim & Chia to be company’s auditor to audit FS for YE 31.3.

Violated. This may create a self-review threat as they will be auditing FS that they were involved in preparing before. They might be biased in issuing audit opinion 9. Rahim & Chia appointed as auditor of K Bhd for YE 31.12 but not reappointed again after that. Immediately after AGM in 2016,Rahim & Chia accepted offer to provide tax consultancy services

Not violated. There is no issue of independence as the appointment of auditor was made before they provide the tax consultancy services

- Chia bought 2nd hand car worth RM150,000 from audit client. The company offered 50% discount and Chia accepted.

Violated. This may create threat to independence/self-interest threat as the purchase was not made on normal term. Chia might be biased in issuing audit opinion 11. Haikal just graduated with Bachelor in Accountancy. He has accepted offer as branch manager in an accounting firms

Violated. Under method of practice, any branch of accounting firm should be under management and control by a person who is a member of MIA

POINTS TO PONDER:

Factors that auditors can violate MIA By-Law:

- THREATS – a) SELF-INTEREST, b) SELF-REVIEW, c) ADVOCACY, d) FAMILIARITY and e) INTIMIDATION

If your answer is VIOLATED, these are suggested points:

THIS MAY CREATE _______________ THREAT AS [RELATE TO QUESTION]. [NAME OF THE AUDITOR] MIGHT BE BIASED IN ISSUING AUDIT OPINION.

- ISSUE OF INDEPENDENCE Suggested reason:

THIS MAY CREATE THREAT TO INDEPENDENCE AS [RELATE TO QUESTION]. [NAME OF THE AUDITOR] MIGHT BE BIASED IN ISSUING AUDIT OPINION.

- FAIL TO COMPLY WITH AREA 100: FUNDAMENTAL PRINCIPLE

Suggested reason:

UNDER [i. CONFIDENTIALITY], auditor has LEGAL/PROFESSIONAL DUTY TO DISCLOSE SUCH INFORMATION. HOWEVER, AUDITOR [RELATE TO QUESTION]

- FAIL TO COMPLY WITH AUDIT FEE REQUIREMENT Suggested reason:

UNDER AUDIT FEE, AUDIT FEE SHOULD REFLECT VALUE OF AUDIT WORK PERFORMED. HOWEVER, AUDITOR [RELATE TO QUESTION]

OR UNDER AUDIT FEE, AUDITOR SHALL REFUSE APPOINTMENT IF THERE IS OVERDUE AUDIT FEE FOR 2 OR MORE CONSECUTIVE YEARS. HOWEVER, AUDITOR _________________

- FAIL TO COMPLY WITH METHOD OF PRACTICE REQUIREMENT

Suggested reason:

UNDER METHOD OF PRACTICE, TO PRACTICE AS A CHARTERED ACCOUNTANT[AUDIT PARTNER, AUDIT FIRM BRANCH MANAGER] HE MUST BE A MEMBER OF MIA. IN THIS CASE, HE IS NOT A MEMBER OF MIA AND ACCEPTED THE OFFER

- FAIL TO COMPLY WITH REFERRAL FEE/COMMISSION REQUIREMENT

Suggested reason:

UNDER REFERRAL/COMMISSION, ACCEPTING REFERRAL FEE MAY CREATE SELF-INTEREST THREAT. [NAME OF AUDITOR] MIGHT BE BIASED IN ISSUING AUDIT OPINION.

Tips MIA By Law / its easy and catchy feel free to download

Course: Auditing (AUD339)

University: Universiti Teknologi MARA