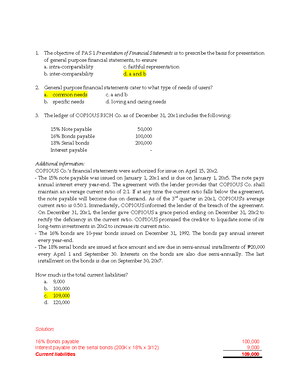

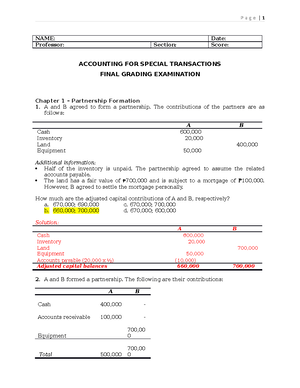

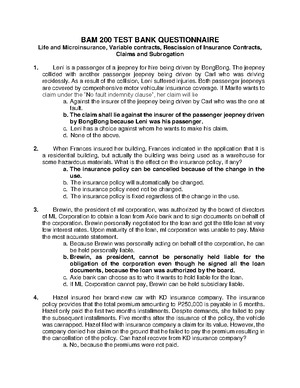

- Information

- AI Chat

Accounting FOR BOT

Accounting 1 (ACC 1)

Northern Bukidnon State College

Related Studylists

Advanced Accounting - Special TransactionsPreview text

ACCOUNTING FOR BUILD-OPERATE-TRANSFER (BOT)

Build-Operate-Transfer (BOT) is a type of project financing model in which a private entity builds and operates a facility or infrastructure project, such as a power plant or a toll road, for a set period of time, after which ownership of the project is transferred to the government or other public entity. Accounting for BOT projects involves several key considerations.

Capitalization: The initial costs of building the facility or infrastructure project are capitalized and recorded as a long-term asset on the balance sheet. These costs may include construction, engineering, and equipment expenses.

Depreciation: The asset is depreciated over the period of time in which it is expected to generate revenue, using an appropriate depreciation method. The amount of depreciation is recorded as an expense on the income statement.

Operating expenses: The private entity is responsible for operating and maintaining the facility during the period of the BOT agreement. Operating expenses, such as salaries, utilities, and maintenance costs, are recorded as expenses on the income statement.

Revenue recognition: The private entity generates revenue from operating the facility or infrastructure project, such as toll fees or electricity sales. Revenue is recognized as it is earned, typically on a monthly or quarterly basis.

Transfer of ownership: When the BOT agreement ends and ownership of the project is transferred to the government or public entity, the asset is reclassified from a long-term asset to a current asset, and any remaining book value is transferred to the new owner.

It's important to note that accounting for BOT projects can be complex and may require the expertise of a specialized accounting team. Additionally, the specific accounting treatment will depend on the terms of the BOT agreement and the applicable accounting standards in the relevant jurisdiction.

Here are some additional accounting considerations for BOT projects:

Financing: The private entity may need to obtain financing to fund the construction of the facility or infrastructure project. The accounting treatment for any loans or other financing arrangements will depend on the terms of the agreement and the applicable accounting standards.

Contingent liabilities: The private entity may be responsible for certain contingent liabilities, such as environmental cleanup costs or legal claims, even after the

ownership of the project is transferred to the government or public entity. These liabilities should be disclosed in the financial statements.

Impairment: If the value of the asset is determined to be less than its carrying amount, an impairment loss should be recognized on the income statement.

Taxes: The private entity may be subject to various taxes, such as income tax, value-added tax, and property tax, depending on the jurisdiction in which the project is located.

Disclosure: BOT projects can involve significant risks and uncertainties, including political, economic, and regulatory factors. It's important to provide comprehensive and transparent disclosures in the financial statements to help stakeholders understand the nature and extent of these risks.

Overall, accounting for BOT projects requires careful consideration of a range of financial, legal, and operational factors, and may involve the use of specialized accounting expertise.

features of bot arrangements

Project financing: BOT arrangements involve private financing of public infrastructure projects, where a private entity, known as the project company, typically finances, constructs, operates, and maintains the infrastructure project. This allows the public sector to access much-needed capital without incurring debt or diverting resources from other public programs.

Time-bound contracts: BOT arrangements are typically based on long-term, time-bound contracts, which specify the terms and conditions of the project, including the duration of the arrangement, the financial obligations of the parties, and the allocation of risk between the public and private sectors.

Transfer of ownership: At the end of the BOT arrangement, ownership of the infrastructure project is typically transferred to the public sector entity. This ensures that the public sector ultimately gains ownership and control of the infrastructure, while the private sector benefits from the opportunity to operate the project and generate a return on investment.

Risk allocation: One of the key features of BOT arrangements is the allocation of risk between the public and private sectors. In general, the private sector assumes many of the construction, operating, and performance risks, while the public sector retains ownership and regulatory risk.

Revenue generation: The private sector generates revenue from the infrastructure project during the BOT arrangement, typically through the sale of services or the

infrastructure projects, including toll roads, power plants, water treatment facilities, and ports, among others. The scope of a BOT arrangement is typically designed to ensure that the public sector gains access to much-needed infrastructure while the private sector benefits from the opportunity to operate the project and generate a return on investment.

accounting issues There are several accounting issues that arise in Build-Operate-Transfer (BOT) arrangements, including:

Revenue recognition: The private entity generates revenue from the infrastructure project during the BOT arrangement, typically through the sale of services or the collection of user fees. The accounting treatment for revenue recognition will depend on the nature of the services provided and the terms of the BOT contract.

Construction costs: The private entity is responsible for constructing the infrastructure project, and the accounting treatment for construction costs will depend on the nature and complexity of the project, as well as the specific terms and conditions of the BOT contract.

Depreciation and amortization: The private entity is responsible for maintaining and operating the infrastructure project during the BOT arrangement. The accounting treatment for depreciation and amortization will depend on the useful life of the asset and the specific terms and conditions of the BOT contract.

Financial reporting: BOT arrangements involve complex financial arrangements and may require specialized financial reporting. Financial statements must be prepared in accordance with applicable accounting standards and should accurately reflect the nature and scope of the BOT arrangement.

Taxation: BOT arrangements may involve complex tax issues, including income tax, value-added tax, and property tax. The accounting treatment for taxes will depend on the jurisdiction in which the infrastructure project is located and the specific terms and conditions of the BOT contract.

Impairment: If the value of the asset is determined to be less than its carrying amount, an impairment loss should be recognized on the income statement.

Disclosure: BOT arrangements can involve significant risks and uncertainties, including political, economic, and regulatory factors. It's important to provide comprehensive and transparent disclosures in the financial statements to help stakeholders understand the nature and extent of these risks.

Overall, accounting for BOT arrangements requires careful consideration of a range of financial, legal, and operational factors, and may involve the use of specialized accounting expertise.

treatment of the operators rights over the infrastructure In Build-Operate-Transfer (BOT) arrangements, the private entity (i., the operator) typically has certain rights over the infrastructure during the term of the BOT arrangement. These rights can include the right to operate and maintain the infrastructure, the right to collect user fees or other revenue generated by the infrastructure, and the right to use and access the infrastructure in accordance with the terms of the BOT contract.

The accounting treatment of the operator's rights over the infrastructure will depend on the nature and scope of these rights, as well as the specific terms and conditions of the BOT contract. In general, the operator's rights over the infrastructure will be reflected in the financial statements as assets and liabilities, as follows:

Assets: The operator may have certain assets related to the infrastructure, such as the right to use or access the infrastructure, or the right to collect user fees or other revenue generated by the infrastructure. These assets will typically be recognized on the balance sheet as intangible assets.

Liabilities: The operator may also have certain liabilities related to the infrastructure, such as the obligation to operate and maintain the infrastructure in accordance with the terms of the BOT contract. These liabilities will typically be recognized on the balance sheet as obligations or provisions.

The specific accounting treatment of the operator's rights over the infrastructure will depend on a range of factors, including the nature and scope of the infrastructure project, the terms and conditions of the BOT contract, and applicable accounting standards. It's important to ensure that the financial statements accurately reflect the nature and extent of the operator's rights over the infrastructure, as well as any related assets and liabilities.

recognition and measurement of arrangement The recognition and measurement of a Build-Operate-Transfer (BOT) arrangement will depend on the specific terms and conditions of the contract, as well as the applicable accounting standards. In general, the accounting treatment for a BOT arrangement will involve the following steps:

Initial recognition: The initial recognition of a BOT arrangement typically involves recognizing the construction costs incurred by the private entity in constructing the infrastructure project as an asset on the balance sheet. The amount recognized will

accounting standards. In general, the accounting treatment for the construction of upgrade services will involve the following steps:

Initial recognition: The initial recognition of the construction of upgrade services will typically involve recognizing the construction costs incurred by the private entity as an asset on the balance sheet. The amount recognized will typically be equal to the cost of construction plus any additional costs incurred by the private entity in preparing the upgrade services for operation.

Depreciation and amortization: The private entity is responsible for maintaining and operating the upgraded infrastructure during the BOT arrangement, and will typically be required to depreciate or amortize the construction costs over the useful life of the asset. The accounting treatment for depreciation and amortization will depend on the useful life of the asset and the specific terms and conditions of the BOT contract.

Revenue recognition: The private entity will recognize revenue from the upgraded infrastructure project during the term of the BOT arrangement, typically through the sale of services or the collection of user fees. The accounting treatment for revenue recognition will depend on the nature of the services provided and the terms of the BOT contract.

Impairment: If the value of the asset is determined to be less than its carrying amount, an impairment loss should be recognized on the income statement.

Liabilities and provisions: The private entity may have certain liabilities and provisions related to the upgraded infrastructure project, such as the obligation to operate and maintain the infrastructure in accordance with the terms of the BOT contract. These liabilities and provisions will typically be recognized on the balance sheet.

It's important to ensure that the financial statements accurately reflect the nature and extent of the upgraded infrastructure project, as well as any related assets and liabilities. Professional accounting advice should be sought to ensure that the recognition and measurement of the upgraded infrastructure project complies with applicable accounting standards and accurately reflects the nature of the transaction.

financial asset A financial asset is an asset that is in the form of a financial instrument, such as a stock, bond, or derivative, and is held by an individual or organization for the purpose of generating a return on investment or for trading purposes. Financial assets can be classified as either marketable securities or non-marketable securities.

Marketable securities are financial assets that can be easily traded in the financial markets and are typically held by investors for short periods of time. Examples of marketable securities include stocks, bonds, and commercial paper.

Non-marketable securities, on the other hand, are financial assets that cannot be easily traded in the financial markets and are typically held for longer periods of time. Examples of non-marketable securities include private equity, venture capital investments, and real estate.

Financial assets are typically measured at fair value, which is the amount that would be received to sell the asset in an orderly transaction between market participants at the measurement date. Financial assets are recognized on the balance sheet of an individual or organization, and their value may fluctuate over time based on changes in market conditions, interest rates, and other factors.

The accounting treatment for financial assets will depend on the specific type of financial instrument and the applicable accounting standards. For example, investments in stocks and bonds may be classified as either held-to-maturity, available-for-sale, or trading securities, each with their own specific accounting treatment. It's important to seek professional accounting advice to ensure that the recognition and measurement of financial assets complies with applicable accounting standards and accurately reflects the nature of the transaction.

intangible asset An intangible asset is an asset that lacks physical substance and is not a financial instrument. Examples of intangible assets include patents, copyrights, trademarks, brand names, goodwill, and software. These assets are often created through the development of intellectual property, brand recognition, or other forms of intellectual capital.

Intangible assets are recognized on the balance sheet of an individual or organization, and their value may fluctuate over time based on changes in market conditions, customer demand, or other factors. Intangible assets are typically measured at cost or fair value, and their value may be amortized or impaired over time based on their useful life or other factors.

The accounting treatment for intangible assets will depend on the specific type of asset and the applicable accounting standards. For example, a patent may be amortized over its useful life, while goodwill may be subject to an annual impairment test. It's important to seek professional accounting advice to ensure that the recognition and measurement of intangible assets complies with applicable accounting standards and accurately reflects the nature of the asset.

Intangible assets are often valuable to businesses because they can provide a competitive advantage and generate future economic benefits. However, because

Accounting FOR BOT

Course: Accounting 1 (ACC 1)

University: Northern Bukidnon State College

- Discover more from: