- Information

- AI Chat

08.1 SHE notes

Business Administration (BSBA)

Tarlac State University

Recommended for you

Related documents

- FASH257 Study Guide 3 - What is lecture method of teaching? Lecture method is the oldest method of teaching.

- FASH257 Lab 7 - What is lecture method of teaching? Lecture method is the oldest method of teaching.

- Top 18 imports exports around world countries move them most 9 fnl

- Conceptual Framework for research purposes

- the system of rules which a particular country or community recognizes as regulating the actions of its members and which it may enforce by the imposition of penalties. "they were taken to court for breaking the law"

- Problems Challenging Architectural Educationinthe Philippines-Exploring New Teaching Strategiesand Methodology

Preview text

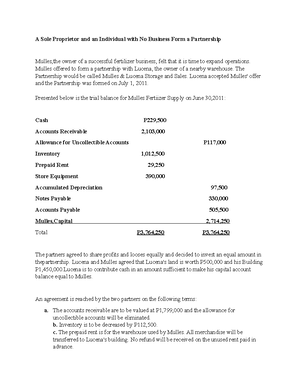

SHAREHOLDERS’ EQUITY

- Authorized capitalization is accounted for using (a) memo method or (b) JE method. The memo method is the more commonly used method. - The excess of issuance price or subscription price over the aggregate par value (stated value) of shares issued or subscribed is credited to the share premium account. - For par value shares, legal capital is the aggregate part value of shares issued and subscribed. For no-par value shares, legal capital is the total consideration received (receivable) from shares issued (subscribed). - Share issuance costs are deducted from share premium. - Treasury shares are an entity’s own shares that were previously issued but are subsequently reacquired but not retired. Treasury shares are accounted for at cost. - Pro-forma entries for Treasury Share transactions (a) acquisition of treasury shares Treasury Shares (at cost) xx Cash xx (b) reissuance of treasury shares at above cost Cash xx Treasury shares (at cost) xx Share premium – TS xx (c) reissuance of treasury shares below cost Cash xx Share premium – TS xx Retained earnings xx Treasury shares (at cost) xx (d) appropriation of RE Retained Earnings – Appropriated xx

Retained Earnings – Unappropriated xx

- Pro-forma entries for Retirement of Shares:

(a) Retirement at below original issuance price Share capital (at part or state value) xx Share premium – original issuance xx Treasury shares (at cost) / Cash xx Share premium – retirement xx

(b) Retirement at above original issuance price Share capital (at part or state value) xx Share premium – original issuance xx Share premium – TS xx Retained Earnings xx Treasury shares (at cost) / Cash xx

- The lump sum price of different classes of shares issued is allocated based on their relative fair values (proportional method). If only one class of shares has a determinable fair value, such class is assigned its fair value and the excess is assigned to the other class with no determinable fair value (incremental method).

- The issuing entity classifies redeemable preference shares as a financial liability. Thus, dividends on these shares are recognized as interest expense.

- Stock rights issued without consideration are recorded through a memo entry. If stock rights are recalled, any consideration paid is debited to “share premium”.

- The conversion feature of convertible preference shares are not accounted for separately. On actual conversion, the convertible preference shares are simply retired and the new shares issued are recognized in the usual manner.

- Stock dividends payable is an adjunct equity account, not a liability account. - Share dividends, share splits, and recapitalization do not affect total shareholder’s equity. - Treasury shares declared as dividends are accounted for at cost. - Noncumulative preference shares are entitled only to current-year dividends. Cumulative preference shares are entitled to dividends in arrears. - Nonparticipating preference shares are entitled only to their basic dividends. After they are paid their basic dividends, any excess dividend is paid to the ordinary shareholders. - Fully participating preference shares are entitled to a pro-rate share with the ordinary shares, based on aggregate par values, after both the preference shares and ordinary shares receive their basic dividends. If there is more than one class of preference shares, the basic dividend of ordinary shareholders is computed using the lowest preference dividend rate. - The participation of partially participating preference shares is computed based on the excess of participation rate over the fixed preference dividend rate. - Dividends are disclosed either on the statement in changes in equity or in the notes. - Dividends declared after the end of the reporting period are not recognized as liabilities in the current period. - Quasi-reorganization refers to restatements of accounts, subject to the provisions of relevant regulations, by an entity under financial distress in order to establish a “fresh start” in accounting sense.

BOOK VALUE PER SHARE - BVPS = Equity ÷ Number of shares outstanding - Subscription receivable is not deducted from total shareholders’ equity for purposes of book value per share computation - Where there are two or more classes of share capital, the total shareholders’ equity is allocated to the various classes of shares using the residual equity theory i., (Total SHE – Preference SHE = Ordinary SHE) - Preference shareholders’ equity is equal to the sum of the following: a. Liquidation value or aggregate par value b. All dividends in arrears for cumulative PS; 1-year dividend in arrears for noncumulative PS. If no dividends are in arrears, no dividends are allocated. c. Amount of participation, if preference shares are participating. - If preference shares are participating, ordinary shares are allocated 1-year dividends using the lowest preference dividend rate. - The balance for participation is allocated to the various classes of shares pro rata based on aggregate par values.

OTHER NOTES (CPAR)

Shareholders’ Equity - Authorized minus unissued equals issued share capital plus subscribed share capital less subscription receivable, plus share premium and retained earnings unappropriated and appropriated minus treasury shares at cost equals shareholder’s equity. - Contributed capital or paid in capital equals issued share capital plus subscribed share capital minus subscription receivable plus share premium, excluding retained earnings. - Note that treasury shares should not be deducted in computing contributed capital. Retained Earnings - Stock dividend of 20% or more is charged to RE at par or stated value. - Stock dividend of less than 20% is charged to RE at fair value on the date of declaration or par or stated value, whichever is higher. - Property dividend is charged to retained earnings at fair value of the property on the date of declaration, at year-end and the date of settlement. - The property to be distributed is measured at year-end at the lower between carrying amount and fair value less cost to distribute. - On the date of settlement, the difference between the dividend payable and the carrying amount of the property is gain or loss on distribution of property dividend. - Items directly affecting unappropriated RE include prior period errors, net income or loss, dividends declared or paid, changes in accounting policy, realization of revaluation surplus and appropriated retained earnings.

**Share Options

- Fair value** of share options on the date of grant is recognized as total compensation. - The total compensation is allocated over the vesting period. If the share options vest immediately , the total compensation is recognized immediately. - Intrinsic value of share options is measured at every year-end until the date of settlement. - Share appreciation rights – The liability for the compensation is equal to the excess of the market price of the share over a predetermined price. Such liability is measured at every year-end until the date of settlement.

AUDIT OBJECTIVES

RECALL: ASSERTIONS

Confirm subscription receivable and consider collectability = usually already is being handled by the TA or corporate secretary

Review AOI, minutes of BOD and Shareholders’ meetings = reviewing minutes of BOD/shareholders meeting provides information as well on other balances/transactions/disclosures

Determine propriety of FS presentation and adequacy of disclosures

08.1 SHE notes

Course: Business Administration (BSBA)

University: Tarlac State University

- Discover more from:

Recommended for you

Students also viewed

Related documents

- FASH257 Study Guide 3 - What is lecture method of teaching? Lecture method is the oldest method of teaching.

- FASH257 Lab 7 - What is lecture method of teaching? Lecture method is the oldest method of teaching.

- Top 18 imports exports around world countries move them most 9 fnl

- Conceptual Framework for research purposes

- the system of rules which a particular country or community recognizes as regulating the actions of its members and which it may enforce by the imposition of penalties. "they were taken to court for breaking the law"

- Problems Challenging Architectural Educationinthe Philippines-Exploring New Teaching Strategiesand Methodology