- Information

- AI Chat

Was this document helpful?

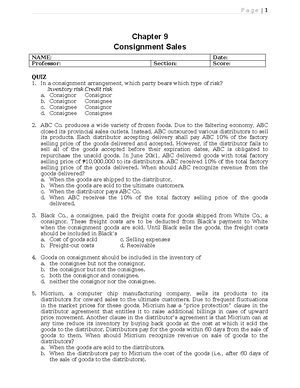

Chapter 14-17 - Hbchh

Course: Accounting (ACC 156)

180 Documents

Students shared 180 documents in this course

University: University of Iloilo - PHINMA

Was this document helpful?

Chapter 14/Firms in Competitive Markets 263

Chapter 14: SOLUTIONS TO TEXT PROBLEMS:

Quick Quizzes

1. When a competitive firm doubles the amount it sells, the price remains the same, so its

total revenue doubles.

2. The price faced by a profit-maximizing firm is equal to its marginal cost because if price

were above marginal cost, the firm could increase profits by increasing output, while if

price were below marginal cost, the firm could increase profits by decreasing output.

A profit-maximizing firm decides to shut down in the short run when price is less than

average variable cost. In the long run, a firm will exit a market when price is less than

average total cost.

3. In the long run, with free entry and exit, the price in the market is equal to both a firm’s

marginal cost and its average total cost, as Figure 1 shows. The firm chooses its quantity

so that marginal cost equals price; doing so ensures that the firm is maximizing its profit.

In the long run, entry into and exit from the industry drive the price of the good to the

minimum point on the average-total-cost curve.

Figure 1

Questions for Review

1. A competitive firm is a firm in a market in which: (1) there are many buyers and many

sellers in the market; (2) the goods offered by the various sellers are largely the same; and

(3) usually firms can freely enter or exit the market.

2. Figure 2 shows the cost curves for a typical firm. For a given price (such as P*), the level

Discover more from:

- Discover more from: