- Information

- AI Chat

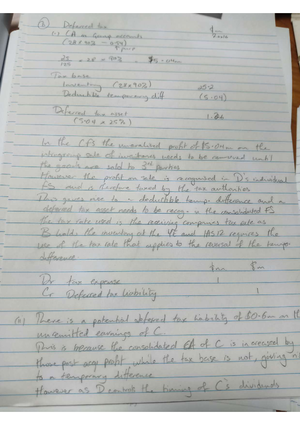

1557 - question paper

question paper

Course

Association chartered of certified accountant (SBL2020)

33 Documents

Students shared 33 documents in this course

University

London College of Accountancy

Academic year: 2020/2021

Uploaded by:

0followers

16Uploads

6upvotes

Recommended for you

Related documents

Was this document helpful?

1557 - question paper

Course: Association chartered of certified accountant (SBL2020)

33 Documents

Students shared 33 documents in this course

University: London College of Accountancy

Was this document helpful?

Redrafted ISA 300

IAASB Main Agenda (October 2005) Page 2005·2201

ISA 300 (Redrafted) (Mark-up showing changes from September)

PLANNING AN AUDIT OF FINANCIAL STATEMENTS

CONTENTS

Paragraphs

INTRODUCTION

Scope of this ISA........................................................................................................................... 1

Effective Date................................................................................................................................ 2

OBJECTIVE TO BE ACHIEVED............................................................................................. 3

REQUIREMENTS

Involvement of Key Engagement Team Members......................................................................... 4

Preliminary Engagement Activities............................................................................................... 5

Planning Activities......................................................................................................................... 6-10

Documentation.............................................................................................................................. 11

Additional Considerations in Initial Audit Engagements............................................................... 12

APPLICATION MATERIAL

Involvement of Key Engagement Team Members......................................................................... A1-A2

Preliminary Engagement Activities............................................................................................... A3A5

Planning Activities......................................................................................................................... A6-A12

Documentation.............................................................................................................................. A13-A15

Additional Considerations in Initial Audit Engagements............................................................... A16

Appendix: Examples of Matters the Auditor may Consider in Establishing the Overall Audit Strategy

Agenda Item 4-G

Page 5 of 16

Discover more from:

- Discover more from: